Amazon Echo schlägt Wellen

Netzwerklautsprecher mit integriertem Personal Assistant

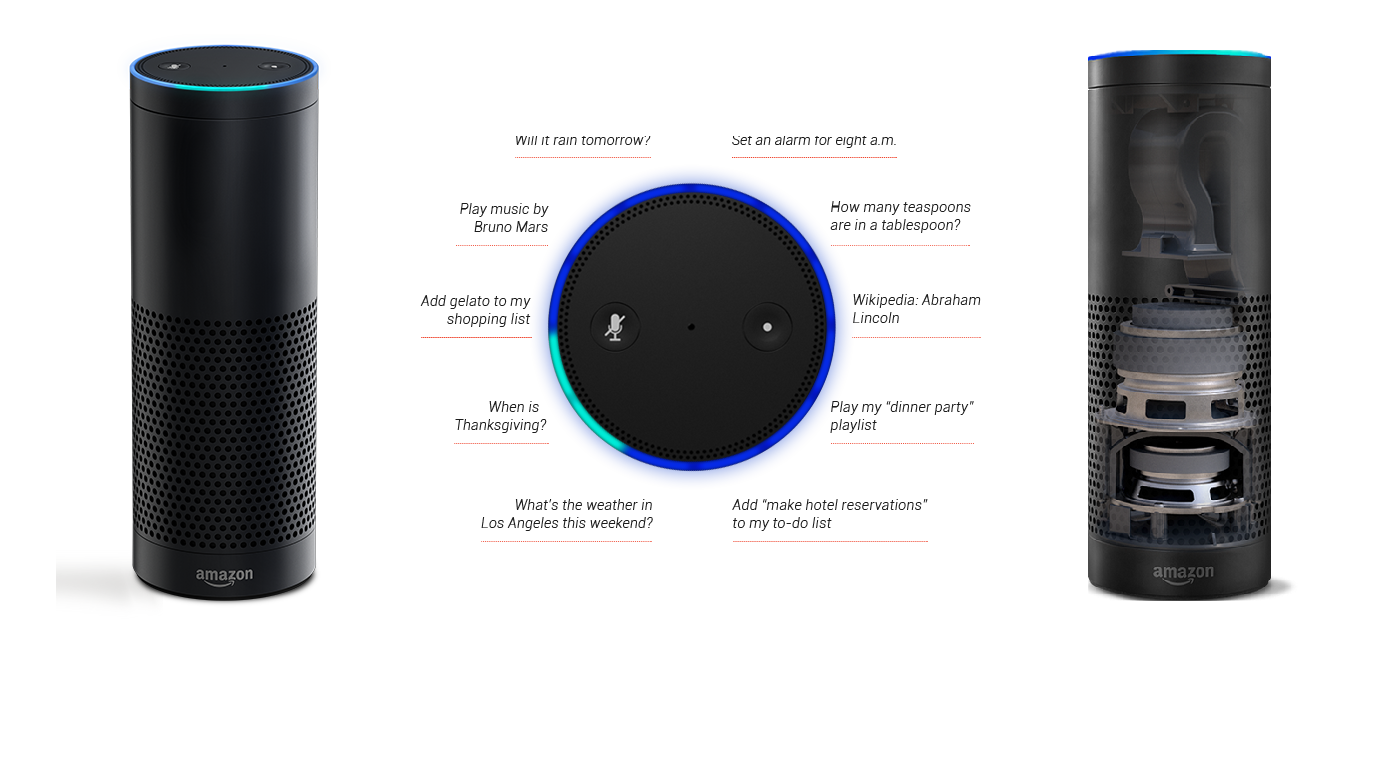

Bild: Amazon.com

Amazon hat überraschend „Echo“ vorgestellt, einen Netzwerklautsprecher, der nicht nur Musik abspielt, sondern permanent lauscht und auf Zuruf Fragen beantwortet, die Todo-Liste ergänzt und mehr.

Die knapp 24 cm hohe schwarze Röhre mit einem Durchmesser von 8,3 cm „Amazon Echo“ ist einerseits ein über Bluetooth und WLAN verbundener Netzwerklautsprecher, der sich von Smartphone oder Tablet mit Musik von iTunes, Pandora und Spotify beschicken lässt. Andererseits wartet der mit Fernfeldmikrofonen und Spracherkennung ausgerüstete Echo auf Sprachkommandos. Dabei betont Amazon in dem Werbespot, dass man Echo nicht anbrüllen muss, sondern „überall im Raum gehört“ wird. Wie Apples „Siri“ und Googles „Ok, Google“ aktiviert ein offenbar wählbares Keyword – im Video „Alexa“ – den integrierten Personal Assistant. Alternativ soll man den Echo offenbar mit der dem Amazon Fire TV beiliegenden Voice Remote mit Mikrofontaste steuern können.

Laut Amazon gibt Echo Auskunft über das Wetter, buchstabiert Wörter, stellt den Wecker, spielt die Lieblingsmusik, rezitiert Wikipedia-Einträge, fügt der Einkaufsliste Einträge hinzu und so weiter. Das „Hirn“ von Echo sind die Amazon Web Services, über die ständig neue Kommandos ergänzt werden sollen.

Hochwertige Bass-Lautsprecher (2,5 Zoll) mit Bassreflex und Hochtöner (2 Zoll) versprechen klaren und verzerrungsfreien omnidirektionalen Klang. Über die Sprachsteuerung sollen sich Amazon (Prime) Music, iHeartRadio und TuneIn steuern lassen, während Musik von Spotify, iTunes und Pandora nur über Bluetooth von Mobilgeräten aus übertragen werden.

Amazon Echo gibt es vorerst nur in den USA zum Preis von 199 US-Dollar; Prime-Kunden müssen nur 99 US-Dollar bezahlen. Noch kann aber nicht jeder Echo kaufen. Interessenten müssen sich bewerben und bekommen eine Mail von Amazon, falls das Los auf sie fällt.

Fans von „Star Trek: The Next Generation“ („Computer … !?) werden ihre Freude an dem Gerät haben, wenn Echo das verspricht, was der Werbeclip von Amazon suggeriert. Auf Privatsphäre bedachte Naturen werden hingegen einen großen Bogen um den Lautsprecher machen und keinesfalls eine Amazon-Wanze im Wohnzimmer dulden – Microsoft kann ein Lied davon singen, man erinnere sich an das Horch und Guck der Xbox One. Ob es da hilft, dass Echo einen Schalter zum Deaktivieren des Mikrofon-Arrays besitzt, ist fraglich.

Doch was bezweckt Amazon mit dem Echo? Es wird ja kaum darum gehen, Eric Schmidt bloß zu beweisen, dass Amazon tatsächlich Googles größter Konkurrent ist. Sollte es wie beim Kindle (Fire) oder Fire TV (Stick) vor allem darum gehen, Amazons Inhalte besser an die Kunden zu bringen – also Bücher, Videos und Musik? Wohl kaum. Im Endeffekt dürfte es darum gehen, den Nutzern den perfekten Shopping-Assistenten an die Seite zu stellen, der die ausgesprochenen Wünsche direkt in dem Amazon-Einkaufskorb platziert …

Das liegt wohl an den grundverschiedenen Voraussetzungen. Star Trek

spielt aus menschlicher Sicht in einer Zukunft, in der die Existenz

des Individuums (zumindest der Spezies Mensch) ganz

selbstverständlich durch die allgemeinverfügbare Technik gesichert

ist. An der Stelle läßt sich die Technik wirklich nur noch gemäß der

Überzeugung der Spackeria (die sind seit NSA auch recht still

geworden) im Rahmen von Peinlichkeit gegen andere einsetzen. Heute

geht es dagegen darum, das Individuum bis an die Grenze der

(ökonomischen) Existenzfähigkeit auszupressen – und manchmal auch

darüber hinaus! (Source: http://www.heise.de/newsticker/foren/S-Re-Reaktion-der-Science-Fiction-Fans/forum-287951/msg-26049853/read/)

Die Zeit ergänzt: http://www.zeit.de/wirtschaft/2014-10/absolute-preisdiskriminierung

Jeder hat seinen Preis

Unendlich viele Preise für ein Produkt: Einer der größten kapitalistischen Träume ist gerade dabei, in Erfüllung zu gehen. Big Data macht es möglich

Supermarkt | © dpa

Die Zeichen dafür, dass sich das kapitalistische Nirwana nähert, mehren sich. Florian Stahl sieht sie überall. Beim Einkauf im Netz, in den USA, in Deutschland. Beispielsweise kürzlich in New York, als sich der Professor für quantitatives Marketing an der Universität Mannheim bei Booking ausloggte, die Cookies löschte, dann seine Hotelanfrage noch einmal startete, diesmal anonym. Da war das gleiche Zimmer plötzlich günstiger. Weil der Algorithmus ihn nicht mehr identifizieren konnte, schlug er ihm einen anderen Preis vor. „Die Preismechanismen sind dabei, sich zu ändern“, sagt Stahl, „und zwar fundamental“.

Im Prenzlauer Berg, im Kaiser’s Supermarkt in der Winsstraße, wo sich Berlin früher zum Flirten traf, drängen sich die Kunden vor einem roten Ständer mit einem Bildschirm. Sie halten eine Karte vor den mannshohen Apparat. Weißes Licht streichelt ihre Hände, ihre Extrakarte wird gescannt, ein leises Summen begleitet das Erscheinen des Bons, darauf ihre Preisabschläge. Dann bin ich dran.

Ich checke ein in die Beta-Phase der dritten industriellen Revolution. Bald soll mich der Kaiser’s Algorithmus komplett verstehen, meine Wünsche vorhersagen können, noch aber kennt er mich nicht. Er hat bisher keinen einzigen Kassenzettel von mir gescannt, nur meine neue Extrakarte. Es ist ein Riesenerfolg in der Kundenkarten-Welt: Ein Drittel der Stammkäufer wurde in den ersten zwei Monaten seit der Einführung Nutzer. Mein Ausdruck zeigt „Ihre persönlichen Angebote heute“: Je 20 Prozent Abschlag für Harry Brot (noch nie gehört) und Bärenmarke Alpenfrische Vollmilch (dachte, die machen nur Kaffeesahne); für Barilla Nudeln gibt es 30 Prozent, für Ritter Sport und Lätta Margarine sogar 40.

Jeder zahlt einen anderen Preis

Hannes Grassegger ist Ökonom und schreibt unter anderem für „Brand Eins“, DIE ZEIT oder die „NZZ“. Er hat einen Essay über den Umgang mit dem neuen Datenkapitalismus veröffentlicht: „Das Kapital bin Ich“ | © Kein & Aber | © Kein & Aber

Vor gut hundert Jahren beobachtete Arthur Cecile Pigou, Professor in Cambridge, ein seltsames Phänomen: Er sah ins Herz des Kapitalismus und es war leer. Der Preis, um den sich die Marktwirtschaft als System der freien Preise dreht, existierte in Wahrheit gar nicht. In The Economics of Welfare von 1920 beschrieb Pigou seine Beobachtung im Kapitel Das spezielle Problem der Eisenbahntarife: Für eine identische Leistung, die gleiche Bahnfahrt von A nach B, zahlten Menschen freiwillig verschiedene Tarife, je nach Klasse. Pigou erkannte, was für die Ökonomie heute so elementar ist wie die Unschärferelation für die Physik: Es gibt keinen objektiv richtigen Preis einer Ware. Es gibt einzig persönliche Werteinschätzungen.

„Preisdiskriminierung“ nannte Pigou die Unterscheidung von Menschen nach den Preisen, die sie für das gleiche Produkt zu zahlen bereit sind. Für Händler ist sie eine wunderbare Möglichkeit, mehr für die gleiche Leistung zu kassieren. In der Vollendung der Preisdiskriminierung, der „Preisdiskriminierung ersten Grades“ könnten Anbieter, so Pigou, jedem einzelnen Käufer einen Höchstpreis für die Bahnfahrt setzen – und ihm so alles abnehmen, was er überhaupt zu zahlen bereit ist. Fortan lernte jeder Ökonomiestudent die totale Preisdiskriminierung als den heiligen Gral des Kapitalismus kennen.

An der Kaiser’s Kasse zeige ich die Extrakarte, piep!, registriert. Jeder Kauf verändert meine zukünftigen Preise: Ladenpreis minus persönlicher Rabatt. Erst einmal bin ich auf keines der Angebote eingegangen, weder Lätta noch Ritter Sport. Am Scanner hole ich mir den nächsten Bon. Wieder das gleiche Angebot. Dreimal muss ich da durch. Dann ist der Algorithmus angeblich soweit.

Personalisierte Angebote als letzte Möglichkeit, den Umsatz zu steigern

Fixe Preise schaffen einen versteckten Sozialvertrag, wie einheitliche Krankenkassenprämien. Hinter Einheitspreisen in Supermärkten, Bahnhöfen und Drogerien steckt ein Gesellschaftskonzept: Alle Käufer sollen gleich sein.

Einheitspreise schaffen Gewinner und Verlierer – dem einen ist etwas eigentlich mehr wert, dem nächsten ist es fast zu teuer. So subventionieren wir einander, vom Joghurtkauf bis zur Taxifahrt. Am meisten profitiert der Durchschnittsmensch. Im Massenmarkt seien personalisierte Preise bislang technisch unmöglich, sagt Florian Stahl, weil sie das Wissen über die Wertschätzung des Käufers für ein bestimmtes Produkt zu einem bestimmten Moment voraussetzten. In diese Wertschätzung könne theoretisch alles einfließen, bis hin zur Wetterlage, wie bei Eis oder Jacken. „Den individuellen Höchstpreis zu erkennen, ist eigentlich ein unendliches Problem“, sagt Stahl.

Lange entsprachen Preise im Alltag dem geschätzten Wert dessen, was unterschiedliche Käufer im Schnitt zu zahlen bereit waren. Bis die Computer kamen, das Internet, Facebook, Google, Scanner, Produkt-IDs, In-Store-Cams, Smartphones – ein Arsenal zur Datafizierung von Personen, deren Vorlieben, Verwandtschaftsverhältnissen, Jobs, Bewegungsmustern, Wertvorstellungen. Seit Kurzem gibt es nun Algorithmen, die die Daten zu dynamischen, individuellen Preisen zusammenrechnen können, wie zuerst die Flugpreise, dann die Hotelpreise, die Elektrizitätspreise und so weiter. Jetzt deutet sich an, dass sich alles herunterbrechen lässt auf den Einzelnen. Es ist, als ob ein Märchen wahr würde.

Das Klingelschild ist golden, Oderberger Straße 44, beste Lage im Prenzlauer Berg, direkt neben dem Modeladen Kauf Dich Glücklich. SO1 steht an der Klingel, kurz für Segment of One. Während in den USA mehr als die Hälfte aller Handelsunternehmen mit sogenannten Price Intelligence Verfahren und dynamischen Preisen experimentiert, jeder zwanzigste Preis bereits personalisiert ist, während die Preisschilder in Frankreich zunehmend durch Digitalanzeigen ersetzt werden, ist das Berliner Start-up SO1 einer der ersten deutschen Anbieter für totale Preisdiskriminierung.

Hier arbeiten 15 Statistiker, ITler, Ökonomen. Menschen, die Google und Henkel verlassen haben, um eine Vision Wirklichkeit werden zu lassen. Sie stecken hinter den roten Automaten in derzeit 30 Berliner Kaiser’s Testmärkten. Die Extrakarte sei eigentlich wie ein physischer Cookie, erklärt der junge Chef und Mitgründer Raimund Bau. SO1 trage die absolute Preisdifferenzierung aus dem Netz, wo Amazon oder Zalando längst so arbeiteten, in die Welt. Die Karten hätten eine anonyme Kundennummer, man brauche im Gegensatz zu anderen Kundenkarten keine persönlichen Informationen wie Namen oder Adresse. Darauf ist Bau stolz. Erfasst würden an der Kasse nur Kaufzeit, Produktnummer, Kartennummer und der gezahlte Preis. „Bei uns laufen die Daten aus den Kassen zusammen. Wir können beispielsweise identifizieren, wer ein Pepsikäufer ist, sogar wenn er nie Pepsi bei Kaiser’s gekauft hat.“ Das ergebe sich allein aus der erfassten Kombination gekaufter Produkte. Jedes Produkt sei ein statistischer Hinweis auf andere Produktvorlieben, so wie Weleda-Shampoo auf Bio-Obst hinweist.

Auf Basis der Wahrscheinlichkeiten, die aus Testmärkten bekannt seien, könnten nicht nur Vorlieben errechnet werden, so Bau, sondern auch die persönliche Zahlungsbereitschaft und Preissensibilität. „Wenn wir den Cola-Absatz erhöhen wollen, finden wir heraus, ob Du als Pepsi-Liebhaber für Cola ein potenzieller Kunde bist. Ob Du es wiederholt kaufen würdest, wenn Du es einmal ausprobierst. Wie viel wir Dir zahlen müssten, um Dich zum Cola-Kauf zu bringen.“ Lohne sich der Kunde für Cola, biete man ihm an den roten Automaten genau den passenden Preisnachlass für Cola. Resultat seien individuelle Preise.

Der gläserne Kunde

Heute arbeite SO1 noch mit Bons, bald werde vieles über Apps laufen, sagt Bau. „PayPal, Mastercard, Google arbeiten sicherlich an ähnlichen Methoden.“ Absolute Preisdiskriminierung sei eine weltweite Bewegung, die kaum aufzuhalten sei, weil in gesättigten Märkten wie dem Lebensmittelhandel der Preiswettkampf der einzige Weg sei, den Umsatz zu steigern. „Persil wäscht jetzt noch weißer“ ziehe nicht mehr, sagt Bau. Und altbekannte Promotionen via Coupons oder Rabattmarken hätten aufgrund der Streuung kaum Effekt. Sie würden vor allem von Leuten genutzt, die das Produkt sowieso kaufen würden. Die Extrakarte bringe dagegen pro Nutzer Umsatzsteigerungen im mittleren zweistelligen Prozentbereich. Für Bau eine Win-Win-Win-Win-Situation für Kunde, Händler, Produzent und SO1.

Das will sich auch IBM nicht entgehen lassen. Demandtec heißt die Software des Konzerns. Große Ketten, Lebensmittelhändler, Drogerien oder Baumärkte sollen sie nutzen, um ihre Preise auf Basis von persönlichen Kaufmustern, Konkurrenzpreisen oder anderen Einflüssen ständig zu optimieren. Das ermöglicht verschiedene Preise von Supermarkt zum Onlineshop zum Mobilgerät oder zwischen Gebieten. Eine zweite IBM-Software namens Xtify bietet Techniken, um Kunden jederzeit ortsbezogen mit Angeboten anzusprechen.

Alle Informationen werden zusammengenommen

Viele Geschäfte haben sich derweil zu veritablen Überwachungsdiensten entwickelt. Das Ziel: Kunden bis ins Detail ausforschen. In der Schweiz können die beiden führenden Supermarktketten Migros und Coop 80 Prozent aller Einkäufe Haushalten zuordnen, dank der Kundenkarten. Niemand weiß mehr über die Schweizer, über ihre Allergien, Aufenthaltsorte, Gewohnheiten, Familienstrukturen, Adressen. Bei der US-Kette Safeways nutzt fast die Hälfte aller Kunden eine App, die ihnen im Supermarkt spezifische Nachlässe anzeigt, beruhend auf der eigenen Shoppingvergangenheit. So entstehen personalisierte Preise.

Ich habe Harry Brot und Barilla Nudeln verbilligt gekauft. Die beiden Angebote fehlen jetzt auf dem dritten Ausdruck. Sonst ist alles beim Alten. Noch ein Einkauf, dann kann ich sehen, was der Kaiser’s Algorithmus von mir denkt. Ob er mir Cola anbietet?

„Von der Ernährung über die Mobilität bis zur Energieversorgung sind elementare Bereiche unseres Lebens von den neuen Preismodellen betroffen“, sagt der St. Galler Ökonom und Zukunftsforscher Joël Cachelin. Und diese Preise würden durch uns unbekannte und unüberprüfbare Kriterien bestimmt.

Alles wird verknüpft

Die für den Einzelnen bedrohlichste Möglichkeit wäre künftig die Verknüpfung aller Informationen über Firmen und Netzwerke hinweg. Jede unserer Handlungen und Äußerungen, auch vergangene, würde den Preis beeinflussen, den wir für etwas zahlen. Das Netz würde zu einer Art Credit History, wie Kritiker des neuen Facebook Werbedienstes Atlas befürchten.

In Dänemark bietet der Reiseveranstalter Spies derzeit schon Sonderpreise für Paare an, die in ihren Ferien nachweislich ein Kind zeugen. Der Werbegag ist ein Versuch, mit Preisen einem der größten Probleme Dänemarks zu begegnen: dem Mangel an Nachwuchs. Preise sind eines der wichtigsten Steuerungsmittel unserer Gesellschaft. Sie sind Politik. „Die Zeiten des Sozialvertrags im Preis gehen zu Ende“, sagt Florian Stahl. Zukünftig könnten Menschen sogar Identitäten tauschen, um niedrigere Preise zu zahlen.

Brotpreise starten Revolutionen. Was aber passiert mit einer Gesellschaft, deren Preissystem sich komplett ändert?

Nach dem dritten Einkauf gehe ich zum Automaten, um endlich mein persönliches Angebot zu erhalten. Das Licht des Scanners wärmt meine Hand. Mein Rabatt erscheint mit sanftem Summen. 20 Prozent auf Bärenmarke Milch, 40 Prozent auf Lätta Margarine.

Die Sueddeutsche schließt den Themenblock: http://www.sueddeutsche.de/digital/neues-produkt-echo-amazon-erfindet-den-lauschsprecher-1.2209840

Amazon erfindet den Lauschsprecher

Amazon Echo: Eine Dystopie in Zylinderform.

Die Gebrauchsanweisung für Amazons neues Produkt hat in ihrer deutschen Ausgabe 351 Seiten und erzählt nebenbei noch die Geschichte einer totalitären Diktatur. Es ist das Buch „1984“ von George Orwell – und das wichtigste Instrument in dieser Dystopie ist der Televisor, der bei allen Bürgern zu Hause fest installiert ist. Er hört alles, kann sprechen und dient auch als Fernseher.

Einen kleinen Unterschied gibt es allerdings: Ein Fernseher ist Amazons „Echo“ nicht und es bleibt auch jedem selbst überlassen, ob er die kleine, schicke, schwarze Säule bei sich zu Hause aufstellt, wo sie fortan auf Sprachkommando reagiert und ihrem Besitzer Fragen beantwortet. Wie zum Beispiel: Alexa, wie viel Uhr ist es? Alexa, wie buchstabiert man Mountainbike? Alexa, wie kocht man Bolognese? Das Codewort Alexa aktiviert Echo.

Das Gerät kann all das, weil es permanent mit dem Netz verbunden ist – und weil Echo offenbar alles hört, was um die kleine Säule herum gesprochen wird. Kein Hersteller hatte bislang die Chuzpe, dieses Gerät wirklich zu bauen und anzubieten. Amazon, der Lieferkonzern, hat die Chuzpe, unsere Gesellschaft zu verändern. Wenig innovative Buchhandlungen und Verlage zu ruinieren. Unseren Konsum zu protokollieren. Produkte will der Konzern seinen Kunden künftig per Drohne liefern – Amazon weiß schon, was gut für uns ist. Dieser Konzern also hat den Televisor gebaut. Herzlichen Glückwunsch!

Die Standleitung zu einem Amazon-Server

Und warum auch nicht. Die gesamte Umgebung um uns herum sammelt Daten. Unsere Handys sowieso, unsere Autos, Bankautomaten, Kassen, Kameras, öffentliche wie private, Payback-Karten, Webseiten, die wir besuchen. Dass Echo da so heraussticht, liegt an zwei Aspekten. Erstens: Echo soll im Wohn- und Schlafzimmer stehen. Das Gerät überwacht – oder bereichert – unser zu Hause. Zweitens: Echo ist, wie man es von Amazon kennt und erwartet, ein besonders innovatives Produkt. Es ist ein Wagnis, aber eines das sich lohnen könnte. Echo rückt uns dort näher ans Netz, wo wir bislang konsequent offline sind. Im Wohnzimmer, beim Faulenzen, beim Kochen, beim Schlafen, im Bett. Echo ist, einem Handy nicht unähnlich, die Standleitung unseres Lebens zu einem Amazon-Server. 199 Dollar kostet das Gerät in den USA, bislang können nicht alle Kunden bestellen, Amazon testet noch, wie das neue, ungewohnte Gerät angenommen wird.

Vielleicht hat Amazon deshalb einen betont konservativen Werbespot zu Echo gedreht, der vor allem suggeriert: Echo macht das Leben einfacher. Ansonsten bleibt alles, wie es ist. Vati hört die Nachrichten mit Echo, Mutti kann den neuen Mitbewohner erst nicht richtig bedienen, aber rafft es dann doch noch – so einfach ist Echo! – und kann in Ruhe mit Echos Hilfe kochen. Und es stimmt ja auch: Nicht das Gerät ist das größte Problem, sondern die fehlenden Regeln für das Gerät. Der Zwang, dem Kunden transparent zu zeigen, was mit ihm geschieht, wenn er das Gerät verwendet. Echo ist nämlich nur die Vorderseite des Produktes, das man erwirbt. Den schwarzen Zylinder kann man anfassen, aber für den Kunden nicht greifbar ist der Amazon-Webserver, der mit Echo verbunden ist und der mit jedem Wort, das in Echos Hörweite fällt, dazu lernt. Über den Sprechenden. Über seinen Tonfall, seine Stimmung, seine Wünsche, seine Probleme, seine Hoffnungen, sein Leben.

Daten, die besonders wertvoll sind

Echo sammelt jene Kategorie von Daten, die besonders wertvoll und besonders kritisch ist, nämlich personenbezogene Daten. Und der Service wäre nicht halb so bedenklich, wenn er klar geregelt wäre und für den Nutzer vollkommen transparent wäre, wie und wo seine Daten liegen, wer sie bekommt und was mit ihnen angestellt wird. Aber welchen Gesetzen gehorcht Echo überhaupt? Amerikanischen? Deutschen? Wer hat Zugriff auf die Daten? Was geschieht mit den Profilen, die unweigerlich entstehen, wenn Echo immer lauscht?

Amazon in Deutschland konnte eine entsprechende Anfrage der Süddeutschen Zeitung nicht beantworten und verweist auf die amerikanische Pressestelle, die bislang nicht reagiert hat. Auf der Echo Produktseite, auf der sich bislang nur amerikanische Nutzer um ein Gerät bewerben können, sind die Vorteile von Echo ausführlich erklärt. Der tolle Klang der Lautsprecher, wie genau Echo höre, was gesprochen wird, wie sich Echo mit anderen Geräten verbinden lässt. Der Hinweis zum Datenschutz aber führt nur zur ganz gewöhnlichen Amazon.com-Datenschutzseite, die Allgemeinplätze und Standardtexte für den Nutzer bereithält. Wer Echo besitzt, weiß deshalb tatsächlich nicht, wie ihm geschieht. Vielleicht ist es nochmal an der Zeit, die 351 Seiten der inoffiziellen Gebrauchsanweisung zu lesen.