The recent run-up in Amazon.com’s (NASDAQ:AMZN) stock price inspired me to revisit an old thorn in my side. AMZN is up 12.2% since the beginning of 2013, despite a very tough retail sales environment and despite the fact that California and some other states now collect what is known as „the Amazon tax.“ In addition, a bill to collect a Federal Internet sales tax was reintroduced in Congress two weeks ago: Online sales tax.

With this in mind, I decided to peruse AMZN’s 2012 10-K, something I had not done in years, to see what was going beneath the headline „veneer“ applied heavily to AMZN’s quarterly sales and net income results.

I knew that AMZN was using some controversial accounting methodologies, but when I pulled apart the financial statements and applied some old fashioned financial analysis, what I found with regard to AMZN’s cost structure, cash flow and true profitability was quite shocking. Looking at some income statements, cash flow from operations and balance sheet indicators, some of which Wall Street never discusses – AMZN looks somewhat like a Ponzi scheme. I say this because I believe it is likely that a serious cash problem for AMZN will develop if its sales growth slows down or even goes flat.

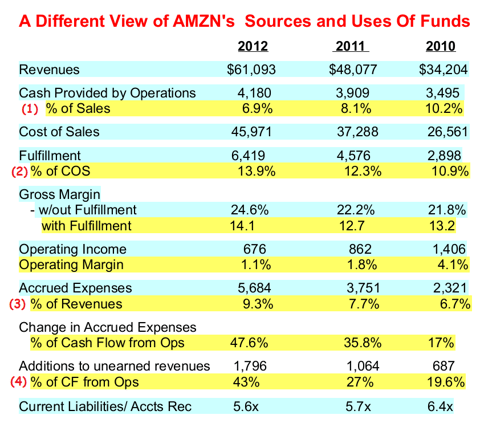

Let’s look at some numbers I put together by „pulling apart“ AMZN’s financial statements from its 2012 10-K (linked for your convenience). I created the table below to focus on what I consider to be the key metrics in understanding the true ability of AMZN’s business model to generate meaningful cash flow. Standard GAAP/adjusted-GAAP accounting statements often use accounting gimmicks that mask true profitability, which I’ll demonstrate below:

First, I wanted to look at cash flow generated by operations. This number is a fairly „clean“ indicator of how profitable the business model is, as it adjusts the reported income for all non-cash charges, adjusts for any non-operating gains/losses and reflects cash required to finance receivables and make vendor financing payments. As you can see, despite robust sales growth over the last three years, the cash generated by each additional dollar of sales is decreasing rapidly, as reflected by the trend shown in line (1) above. While it’s true that a smaller percentage of a growing sales number is still an increase, you can see that from 2011 to 2012 sales jumped by $13 billion but operational cash flow only increased by $271 million. This is a red flag. Please note, this cash flow number does not include AMZN’s big capex program – it’s purely a measure of AMZN’s organic operational profitability

Second, I believe a big part of the declining cash flow margin comes from AMZN’s cost of fulfillment – the cost delivering products to the end-buyer. I have always believed that AMZN’s business model generated tremendous sales growth because AMZN’s fulfillment strategy, in effect, heavily „subsidizes“ the all-in price paid by the customer. As you can see in (2) above, AMZN’s fulfillment costs have increased as a percent of its cost of goods sold in each of the last three years.

In fact, the way AMZN accounts for fulfillment is quite controversial: AMZN’s accounting. AMZN does not include fulfillment costs in its cost of goods sold (COGS), despite the fact that shipping – getting sold products to the buyer – is an integral part of the all-in cost of products sold in AMZN’s business model/strategy. AMZN’s „holy grail“ is that it can sell products over the Internet more profitably than „brick and mortar“ retailers, so the cost of delivery should be part of the cost of sales.

It’s a grey area of FASB rules, but not including this expense in the COGS distorts AMZN’s gross margins vs. that of competitors. (2) in the table above shows AMZN’s gross margin with and without fulfillment costs. As you can see from the difference in the two metrics, AMZN is heavily incentivized to keep the cost of fulfillment out of its COGS calculation. Gross margin is a key metric for analyzing profitability. In 2012, Target’s (NYSE:TGT) gross margin was 31%, Wal-Mart’s (NYSE:WMT) was 25% and Best Buy’s (NYSE:BBY) was 24.6%. You can see why AMZN has refused to consider fulfillment costs as part of the cost of a product, despite the fact that it is a key component in generating revenue. Fulfillment costs have been a rising part of AMZN’s overall product cost. As the cost of energy, and there the cost of shipping, increases it will put even more of a squeeze on the cash margin AMZN earns with each sale.

Third, AMZN’s operating margin is razor thin compared to its comparables. You can see from (3) in the table above that it’s been deteriorating quickly over the last three years. For 2012, TGT and WMT had operating margins of 7.6% and 5.6%, respectively. Remember, AMZN’s theory with its business model is that it can operate less expensively than its „brick and mortar“ rivals. The numbers for the last three years suggest that AMZN fails to deliver on this.

Let’s now look a little more deeply at the cash being generated by AMZN’s operations and why I believe AMZN resembles more of a Ponzi scheme than people realize. In addition to cash being generated by sales, „cash provided by operations“ also includes changes in working capital. Inventory is a use of cash; accounts receivable, accounts payable and other current liability accruals are sources of cash.

Retailers tend to have a much larger amount of accounts payable than they do receivables. Cash comes immediately from sales and companies negotiate payment terms from vendors, etc, thereby giving retailers the „float“ on cash generated by operations. In order for this model to work, it is important for sales to grow over time, as the „velocity“ of „cash in“ needs to stay ahead of the velocity of „cash out,“ otherwise a liquidity problem can develop.

I chose to isolate and focus on AMZN’s accrued expenses because the payables have been increasing at a normal rate. However, the accrued expense account (3) has been increasingly a significant portion of AMZN’s „cash provided by operations,“ – its „cash in.“ As you can see from the table above, accrued expenses are growing and have gone from just 17% of cash flow from operations to over 47%. This is a big red flag.

Accrued expenses are largely cash from the sale of gift cards. If gift cards go unused, and some do, they accrue 100% to operating income. AMZN doesn’t disclose the other sources of accrued expenses, but it isolates „unearned revenues“ in its cash flow statement (4) – this is gift card cash. As you can see, gift card sales have been a growing source of cash funding over the last three years, representing 43% of cash generated by operations in 2012. If I didn’t know exactly what business AMZN was in, I would be under the impression that it was trying to become a gift card sales operation.

My point here is that – at 43% of cash generated by operations – AMZN is become increasingly reliant on the „float“ it gets from gift cards in order to fund its operations on a short term basis. If AMZN’s revenues slow down or its expenses unexpectedly increase, for whatever reason, AMZN could face liquidity problems.

What happens if sales slow down because of a bad economy or predatory competitors? On Monday (March 3) Wal-Mart announced that it was going to start going after AMZN’s „Marketplace“ web vendor business: Wal-Mart/Amazon. This will likely „cannibalize“ AMZN’s „net service sales,“ which has gone from 10% of revenues to nearly 15% over the last three years. AMZN doesn’t break out its income from its revenue segments, but its Marketplace business is likely very high margin, meaning it’s become an important part of cash generated by operations. In addition, the imposition of the internet „Amazon tax“ will increase the customer’s all-in cost to buy from AMZN, which could significantly impact sales negatively.

AMZN’s market cap as of the 3/7/2013 close is $124.5 billion. Based on 2012 operating income, it’s trading at 185x operating income. For comparison purposes, WMT and TGT trade respectively at 9.2x and 8x their 2012 operating income. The p/e comparison is irrelevant because AMZN lost money on a net income basis in 2012, but that multiple of cash flow unequivocally represents an irrational „bubble“ valuation.

AMZN’s market cap has always been one of the unsolved mysteries of the stock market. Moreover, in its entire operating history, AMZN has never generated meaningful income or cash flow. It is clearly highly overvalued relative to its peers. But, I have rarely made money either shorting the stock or buying puts. It’s been a long-time source of frustration and at this point I’m going to wait until I see the signs that the Ponzi-like cash funding scheme AMZN has in place starts to deteriorate and then I’m going to pounce hard on the short side. Given that retail sales seem to be slowing down – and by some metrics declining – with the economy, and given that Wal-Mart is going to start throwing its weight around at one of AMZN’s key sources of cash flow, I don’t think I’ll have to wait much longer.