What’s happening is pretty simple. The hardware and the software running on any device itself have become way less interesting than the web apps and services, like the ones that Google and Amazon have made the core of their business.

Why buy a $700 iPhone when a $200 Android phone can access the same YouTube or Amazon Music as everyone else? All you need to do to get new Facebook features is refresh your browser or update your app. You don’t need a high-performance device to participate in the 21st century.

It’s a stark contrast with the traditional model for consumer electronics, where you’re expected to upgrade the hardware to keep pace with the new features they release.

And it could be a dire omen for high-margin hardware companies like Apple.

Meanwhile, web-first companies like Amazon and Google are more than happy to exploit this, even as our notions of what a computer actually is continue to shift. Just look at devices like Google Chromecast and the Amazon Echo.

The real brilliance of the Chromecast lies in what it isn’t, rather than what it is. It doesn’t have an interface of its own. You just push a button on your phone and have whatever YouTube video you’re watching or Spotify album you’re listening to appear on your TV screen.

A nice side effect: It’s relatively simple to take an existing smartphone app and add Chromecast streaming capabilities, and literally tens of thousands of apps have done that integration.

You don’t have to think about it or learn a new interface; you just click and go.GettyAmazon VP of Echo Mike George.

It means that every single day, I get more return on the initial $35 investment in the Chromecast I bought in 2014. But since all of the good stuff is happening in the apps, not the Chromecast itself, it’s extremely unlikely that I will ever have to replace this Chromecast, barring a hardware malfunction.

You could probably say the same thing about the Amazon Echo home voice assistant. Developers have released almost 1,000 „skills“ for the Amazon Echo’s Alexa platform, including the ability to call an Uber, play Spotify music, or order a Domino’s pizza.

These gadgets are getting better, not worse, the longer they stay on shelves. And while there may be periodic minor hardware improvements, they’re way more minor than the gap between an iPhone 5 and an iPhone 6, and far less necessary to keep getting maximum value from the device.

The pressure is on

This move is going to keep putting pressure on hardware-first manufacturers — especially those who rely on high margins, like Apple.

The Chromecast and the Echo are relatively cheap gadgets — because all the important, useful stuff about them lives in the cloud, they’re optimized to be small, efficient, and unobtrusive.

TeslaTesla’s autopilot mode scanning the road.

Amazon doesn’t need to make money on the Echo itself, as long as it drives more commerce to its retail business. Same with Google: as long as the Chromecast gets more people to watch YouTube videos and download more stuff from Google Play, they don’t have to make money from the gadget itself.

This trend isn’t going to kill off the smartphone, or the PC, or the tablet. But it means lower-cost gadgetry that lasts a lot longer. We’re only seeing the early stages of this shift now, but it has a lot of potential to shake up how we think about and how we buy our devices.

During Amazon’s most recent earnings call, Baird Equity Research analyst Colin Sebastian asked two questions to Amazon CFO Brian Olsavky: one about Amazon Web Services‘ margins, and another about the chances of Amazon expanding its own shipping logistics services to other companies.

The first one got answered promptly, though Olsavsky had to stop mid-sentence because the operator accidentally jumped in early. Still, Olsavsky made it a point to get back and finish his answer.

The second question never got answered.

„If he wanted to talk about it, he would have remembered to answer,“ Sebastian told Business Insider. „Either way, I think the answer is that Amazon doesn’t talk about potential or future services.“

Amazon’s notoriously secretive about its future plans, so it’s not too surprising that Olsavsky skipped Sebastian’s question.

But when you’re going after something as big as the logistics and shipping market, it’s hard to keep your plans under wraps — and a growing amount of evidence suggests Amazon may indeed be going after the delivery and logistics market, which Sebastian pegs as a $400 billion market opportunity.

Next $400 billion opportunity

Over the past few months, we’ve seen a series of reports speculating Amazon’s plan to establish a bigger in-house logistics service that will allow it to potentially bypass its current delivery partners, like UPS and FedEx.

That includes:

Calling itself a „transportation service provider“ for the first time in its annual report.

Serbastian believes this all points to Amazon building up its in-house logistics delivery network. He envisions Amazon first starting out with its own deliveries, but eventually opening up the service to other companies, putting it in direct competition with the likes of UPS and FedEx.

„Among other opportunities, Amazon has ‚powerhouse potential‘ in the large transportation and logistics market, dominated by global enterprises such as DHL and UPS,“ Sebastian wrote in a recent note.

„Amazon’s cloud technology expertise and increasingly complex fulfillment, logistics and delivery network seem to be obvious foundation to offer third-party services, with an incremental $400-450 billion market opportunity.“

Thomson ReutersWorker gathers items for delivery at Amazon’s distribution center in Phoenix

The report, citing a 2013 Amazon document, revealed an internal project called Dragon Boat, which is intended to become a service that controls everything from picking up the product at the factory in China to delivering it to the end customer in the US.

It said the document described Project Dragon Boat as a „revolutionary system that will automate the entire international supply chain and eliminate much of the legacy waste associated with document handling and freight booking.“

„Sellers will no longer book with DHL, UPS, or FedEx but will book directly with Amazon,“ the report said.

When Amazon’s Olsavsky was asked about its logistics plan again by another analyst during earnings call, he simply shrugged it off as a complementary service, saying it’s intended to supplement, not replace, existing delivery companies.

„What we found in order to properly serve our customers at peak, we’ve needed to add more of our own logistics to supplement our existing partners. That’s not meant to replace them,“ Olsavsky said.

Next AWS

Thomson ReutersVogels, Amazon.com chief technology officer, speaks at the AWS Re:Invent conference at the Sands Expo in Las Vegas

But don’t expect Amazon’s logistics business to expand overnight.

If anything, it’s going to take a few years to fully ramp up and establish itself to become a viable delivery option for other companies, according to Sebastian.

„They will start small, mostly to add capacity for their own business, but then, over time, as they gain more expertise, they will offer extra capacity to other companies,“ Sebastian told us.

In that sense, it could follow the path of Amazon Web Services, its cloud computing service that’s now generating almost $8 billion in annual revenue.

Amazon built AWS out of the infrastructure it had created to support its own operations, but it’s now become one of the most widely used cloud computing platforms, used by everything from small startups to big companies like Netflix and GE.

„I think it’s like AWS,“ Sebastian said. „But it took 10 years for AWS to get as large as it is.“

Darum könnten Mobilfunkanbieter in Zukunft überflüssig werden

In Zukunft wird mobiles Internet so selbstverständlich wie der Strom aus der Steckdose. Gut für die Nutzer, schlecht für die Mobilfunkanbieter, die immer austauschbarer werden.

Weltweit gibt es sieben Milliarden Mobilfunkanschlüsse, davon in Deutschland 112 Millionen . Tendenz steigend. Läuft es also gut bei den Mobilfunkanbietern? Nur für den Moment. In Zukunft werden sie austauschbar, denn schon heute unterscheiden sie sich im Prinzip nur durch Preis, Datenvolumen und Netzabdeckung voneinander. Zusatzdienste, die zu den Anfängen des Mobilfunks für die Nutzer noch eine Rolle spielten, haben keine Bedeutung mehr. In Zeiten von WhatsApp oder iMessage brauchen Nutzer keine teuren SMS-Pakete mehr. Auch die Telefonie wird unwichtiger, was zählt ist die Datenverbindung.

Over-The-Top-Dienste (OTT) wie Skype, WhatsApp, iMessage und Co. legen kontinuierlich zu, während die klassischen Kommunikationsdienste wie Telefonie oder SMS in der Nutzung sinken. Laut der Bundesnetzagentur lag die mobile Datennutzung 2014 im Monatsmittel bei 288 Megabyte und damit viermal so hoch wie noch 2011. Mobil telefoniert wurde in Deutschland 2014 im Monat nur noch knapp 80 Minuten. Drastisch eingebrochen ist auch die SMS-Nutzung : von 60 Milliarden SMS im Jahr 2012 blieben 2014 nur noch 22,5 Milliarden übrig.

Die Kluft zwischen Nutzer und Mobilfunkanbieter wird größer

Gleichzeitig wird die Kluft zwischen Nutzer und Mobilfunkbetreiber immer Größer, wie die Umfrage des Marktforschungsinstituts für Servicequalität zeigt. Das Gesamturteil für die Mobilfunkbranche ist nur befriedigend und an erster Stelle stehen bei der Kundenzufriedenheit die Mobilfunkdiscounter. Die Netzbetreiber Telefonica, Telekom oder Vodafone bilden das Schlusslicht. Die qualitativen Unterschiede zwischen den Netzbetreibern, anfänglich noch deutlich größer, werden immer geringer.

„Es gibt kein wirklich schlechtes Mobilfunknetz mehr.“

Es gibt kein wirklich schlechtes Mobilfunknetz mehr, was auch zur Wechselfreudigkeit beiträgt. Dank der Möglichkeit der Mitnahme der Rufnummer sinkt die Bindung zu einem bestimmten Mobilfunkanbieter. Obwohl die Kluft zum Kunden immer größer wird, unternimmt die Branche viel zu wenig, um den Kunden zu binden. Auf den demografischen Wandel der Nutzer und die damit einhergehende Veränderungen im Nutzungsverhalten wird mit den falschen Maßnahmen reagiert. Die steigende Beliebtheit von Messaging-Diensten wie WhatsApp wurde anfänglich belächelt, bis dann vier Jahre nach dem Start von WhatsApp & Co der zaghafte Versuch unternommen wurde, mit der App Joyn eine Alternative zu bieten. Erfolglos, schaut man sich das Ranking im App-Store und der Anzahl der Bewertungen an.Gleichzeitig untersagen die Mobilfunkanbieter in ihren AGB die Nutzung von Diensten wie P2P (Peer-to-Peer), Instant Messaging oder VoIP (Voice over IP). Kein Problem hat man damit, Streaming-Dienste wie beispielsweise Spotify von der Berechnung des Datenvolumens auszuschließen. Mit Netzneutralität hat das nur noch wenig zu tun. Hauptsache der Rubel rollt. Statt sich auf den Nutzer zu fokussieren, wird selbiger lieber gemolken. So sind in kaum einem anderen Land die Kosten für mobiles Internet so hoch wie in Deutschland. Ist in Finnland ein Inklusiv-Volumen von 50 Gigabyte üblich, steht Deutschland mit einem Gigabyte hinter Italien, Tschechien oder Spanien und nur knapp vor Ungarn. Finde den Fehler.

Der SMS-Killer. WhatsApp läutete den Untergang der SMS ein (Quelle: Twin Design / Shutterstock.com)

Zukunft der Mobilfunkanbieter ist düster

Die Liste der gescheiterten Unternehmungen, eigene Dienste zu etablieren, ist lang. Messaging, Musik-Streaming oder Mobile Payment, allesamt eher klägliche Versuche beim Nutzer zu punkten. Der Zugriff auf den Kunden wird in Zukunft weiter sinken, denn gemeinsam mit der GSM-Association, dem Verband der Mobilfunknetzbetreiber, verhandeln Samsung und Apple über die Einführung der eSim. Bei der eSIM handelt es sich um eine fest verbaute Sim-Karte, auf die jeder Mobilfunkbetreiber aufgeschaltet werden kann. Kunden brauchen in Zukunft keine Sim-Karte mehr für das Smartphone, sondern können sofort loslegen.

Der Wechsel zwischen den Mobilfunkanbietern wird damit entsprechend vereinfacht, da der lästige Wechsel der Sim-Karte entfällt. Die Hoheit der eSim liegt beim Hardware-Hersteller, also bei Apple und Samsung. Das heißt, dass sowohl Apple als auch Samsung einen Mobilfunkbetreiber anbieten, aber eben auch ausschließen können. Mobilfunkanbieter, die besonders restriktiv gegenüber bestimmten Onlinediensten sind, könnten einfach seitens der Smartphone-Hersteller ausgeschlossen werden. Mit der eSim geht ein weiterer Baustein in der Kundenbeziehung für die Mobilfunkanbieter verloren. Und es bröckelt weiter, denn Apple bietet, zunächst nur in den USA, das iPhone als Abo-Modell an.

Für einen Betrag von 39 US-Dollar kann das iPhone gemietet werden und der Kunde bekommt automatisch immer das neueste Gerät. Das Gleiche bietet Samsung auch an und andere Hersteller werden folgen. Mit neuen Smartphones gekoppelt an eine Vertragsverlängerung können die Mobilfunkanbieter künftig also auch nicht mehr locken. Die nicht abreißenden Gerüchte, Apple wolle ein VMNO, ein virtueller Mobilfunkanbieter werden, dürften bei den etablierten Mobilfunkbetreibern nur so mittelgut ankommen. Ganz abgesehen von Projekten wie Googles Loon, dessen Ziel nichts geringeres ist, als die Welt mit Internet auszustatten.

Sri Lanka ist das erste Land, welches mit Hilfe von Google Loon einen landesweiten universellen Internetzugang über WLAN bekommt. Auch wenn Sri Lanka nur eine Insel und nicht Europa ist, sieht man, wohin die Reise bei Google geht. Für Unternehmen wie Google, Facebook oder Apple ist mobiles Internet die Basis für alle Produkte. Die Abhängigkeit von Mobilfunkprovidern ist, wie man am gerade von Google gestarteten Accelerated-Mobile-Pages-Project sehen kann, ein Problem.

Project Loon als Gefahr für den klassischen Mobilfunk? (Foto: Google)

Fazit

Die Frage ist nicht, ob es die Mobilfunkanbieter in Zukunft noch geben wird, sondern viel mehr welche Rolle sie spielen werden. Die Bindung zum Kunden geht zunehmend an Unternehmen wie Apple, Google, Facebook oder Amazon verloren. Ein Ökosystem, wo Kunden Lösungen aus einer Hand bekommen, die nahtlos mit einander funktionieren, ist heute essentiell. Apple, Google, Facebook und Amazon haben das erkannt und bieten genau das: einzelne Lösungen aus einer Hand für unterschiedliche Anwendungsfälle mit Fokussierung auf den Nutzer.

Im Mobilfunk wird das vernachlässigt und es fehlen innovative Ideen und Lösungen. Themen werden entweder zu spät oder nicht nutzerzentriert angegangen, wie man an den Entwicklungen im Bereich Mobile Payment sehen kann. Anstatt sich mit den Kundenbedürfnissen zu beschäftigen, steht am Anfang das Geschäftsmodell. Am Ende bleibt nur noch die Rolle des Technologie-Anbieters, die in etwa so spannend ist wie Strom aus der Steckdose. Gar nicht.

Silicon Valley’s Best Hope for Beating Amazon Is Live

JetJet.com is one of the most buzzed-about companies in Silicon Valley, raising $255 million even before launching to the public. And yet its mission seems doomed from the start: to compete with Amazon in online retail.

But you have to give Jet credit for a strategy that, however sophisticated the machinery underlying it, sticks to the basics. Jet thinks it can win by saving you money.

The long-awaited startup is coming out of beta and launching its online marketplace today with the promise to get you the best price for any product you want to buy. Jet wants to be the place you think of first when you need to restock everyday stuff—toothpaste, toilet paper, a new speaker, or pretty much anything (besides fresh produce—for now).

Jet

The catch? Similar to Costco or Sam’s Club, you pay a $50 membership fee to Jet each year to have access to its goods. With your card, the company promises low prices and savings, claiming members will save an average of $150 a year.

As a shopper, you already have plenty of options from major megastores—Amazon, Walmart, Costco, Target—to smaller niche retailers online and IRL. You likely already have a favorite place to get discounted electronics or deals on household products.

But Jet thinks it can elbow its way into retail by changing how it works. “We’re trying to do something different in that, pretty much anything you want to buy from TVs to toilet paper, you could get 10-15 percent off what you normally spend, without doing anything other than coming to our site and becoming a member,” Liza Landsman, Jet’s executive vice president and chief customer officer, says.

Now that it’s live, we’ll finally get a chance to see if Jet is the next big thing—or the next big bust.

How It Works

Unlike other online retailers, Jet’s revenue comes only from membership fees, not sales. This gives the company every incentive to charge the lowest price possible for items to get you to sign up.

Jet

Behind the scenes, Jet uses a pricing engine to help you find the lowest price. Let’s say you decide you want to shop for that toothpaste, toilet paper, and shower speaker. On top of its already lower sticker price, the site offers additional savings if you, say, buy the toothpaste and toilet paper from the same retailer, or from the same location. (Jet sells some merchandise itself but mostly acts as a marketplace for third-party sellers.) The company says you can gain additional savings by, for instance, waiving the option for free returns or, eventually, opting for slower delivery.

Earlier this year, Jet founder and CEO Marc Lore told my WIRED colleague Issie Lapowsky that Jet’s tech resembles a real-time financial trading service. With the help of this service, Jet not only allows you to find the cheapest available price for a product but also recalculates your shopping cart as you add more products, applying rules based on what the retailers themselves are offering and showing you in real-time how to get more savings by, say, buying two products together. More stuff may mean more discounts.

For retailers, this set-up might seem like a nightmarish recipe for losing money. But Jet says that it doesn’t undercut retailers since it isn’t itself taking a cut, unlike some other online retailers. In fact, for products that aren’t already in its inventory or from one of its partners, the Wall Street Journal reports that Jet is actually buying products at their regular prices from those outside retailers (and paying for shipping charges) while still offering the discounted price to its customers. At times, Jet is taking the loss, it seems, in the hope that it can keep you coming back.

Jet

Future of Retail

But if Jet is forced to pay the difference to deliver goods to you on the cheap, the company may have a difficult time becoming profitable (this challenge has stymied Amazon for the past two decades). In fact, for Jet to succeed—and to fend off retailers such as Amazon, Walmart, and Costco—it will likely need to prepare for several years of losses, if not more. Jet’s model can only succeed at a huge, huge scale—and to get there, it’ll need lots and lots of people like you.

Of course, that may very well happen. According to Forrester Research, 69 percent of the US online population “regularly buys products online.” This year Americans are expected to spend $300 billion online, a number that will likely only keep on growing. “You’ll see more people adopting e-commerce and buying more,” says eMarketer retail analyst Yoram Wurmser. “There’s a lot of room for growth.”

By appealing to the more frugal side of all of us, Jet and its backers expect this audacious startup can not only save us money, but truly challenge Amazon in the process. “Jet is legitimate. It’s small, it’s a startup, but it’s got a good model,” Wurmser adds. “I think Jet does represent a competitor because they can undercut prices.” And, after all, who doesn’t want cheaper stuff? It just has to solve one of the most tantalizing paradoxes of retail: making more money by letting you pay less.

Amazon is known for having low prices. But a study conducted by a startup called Boomerang Commerce reveals that Amazon’s pricing strategy is much more nuanced than simply undercutting the competition.

Boomerang, founded by Amazon veteran Guru Hariharan, makes software that tracks prices on shopping sites that compete with its clients, then recommends price changes dynamically. Those changes are based on rules its clients set about which products to match prices on and which to boost higher or drop lower than a competitor’s to boost profits or sales, respectively.

The study of Amazon’s pricing uncovered some interesting tactics. First, Amazon doesn’t have the lowest prices across the board, which may not surprise industry insiders but might surprise Amazon shoppers.

Instead, according to Boomerang’s analysis, Amazon identifies the most popular products on its site and consistently prices them under the competition. In one example, Boomerang observed Amazon testing price reductions on a $350 Samsung TV — one of the most popular TVs on Amazon — over the six months leading up to Black Friday. Then, on Black Friday, it dropped the price to $250, coming in well below competitors’ prices.

But when it comes to the HD cables that customers often buy with a new TV, Amazon actually pushed up the price by 33 percent ahead of the holidays. One reason is that the cables weren’t among the most popular in their category, meaning that they have little impact on price perception among shoppers. Secondly, Amazon most likely figures (or knows) it can make a profit on these cables because customers won’t price-compare on them as carefully as they would on more expensive products.

In another example, Amazon priced one of the most popular routers on its site about 20 percent below Walmart’s price. But when it came to a much less popular router, Amazon priced it almost 30 percent higher than Walmart did. Again, Amazon knows which products will drive price perception among shoppers.

“Amazon may not actually be the lowest-priced seller of a particular product in any given season,” the report reads, “but its consistently low prices on the highest-viewed and best-selling items drive a perception among consumers that Amazon has the best prices overall — even better than Walmart.”

The study was part of a white paper Boomerang released on Tuesday to bring attention to the idea of price perception in e-commerce. The startup has created a “price perception index,” which it described as “a numerical pricing model that captures customer psychology of price perception. It does so by providing a tangible statistic of how a company’s products … are priced, relative to the competition, weighted by customer interest.”

The goal of the index is to highlight how a nuanced approach to pricing — such as Amazon’s — can be a smarter, more cost-effective option over simply price-matching across the board. This is where Boomerang enters the conversation: The startup wants to help Amazon competitors think about pricing in as sophisticated a way as Amazon does.

“Amazon is doing it at scale, with what is estimated to be 10 billion pricing changes across the holidays,” CEO Hariharan said. “Some retailers are doing it every three months.”

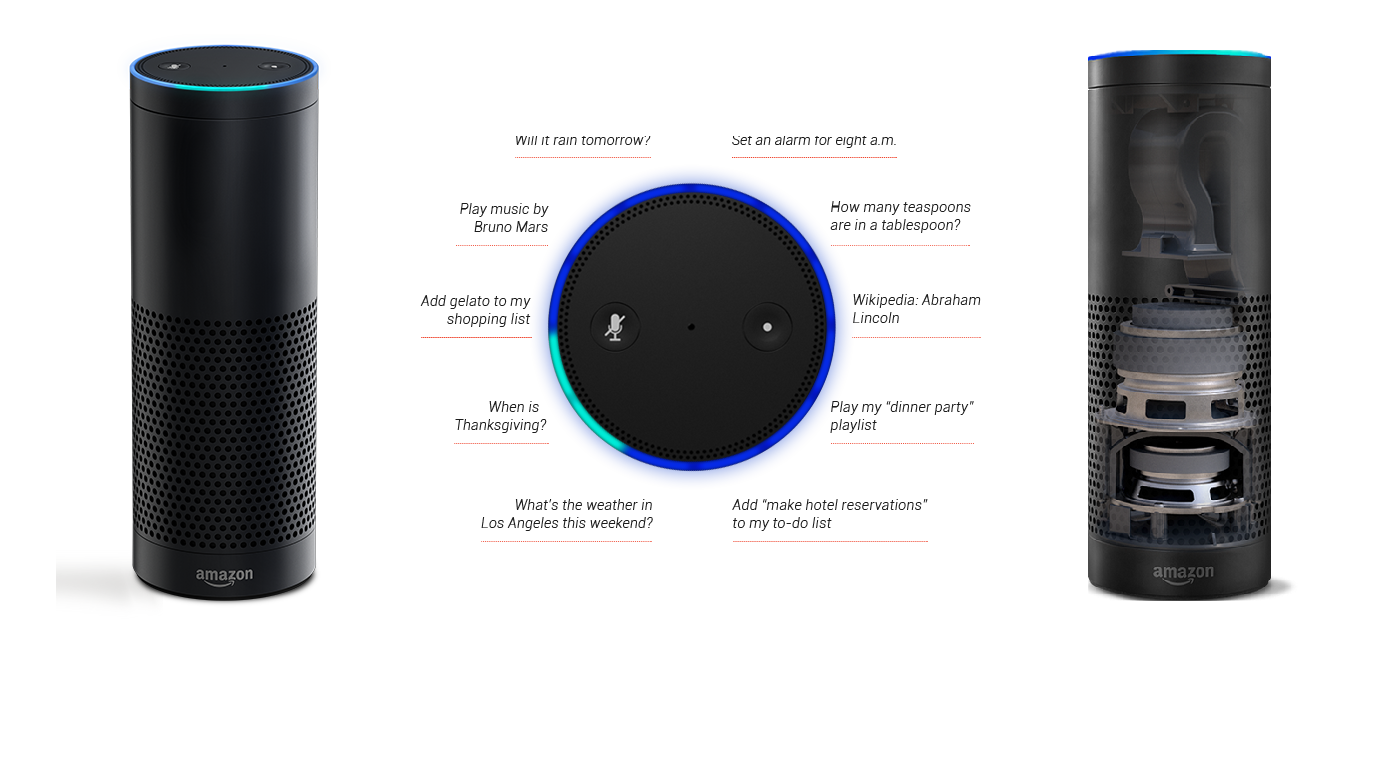

Amazon hat überraschend „Echo“ vorgestellt, einen Netzwerklautsprecher, der nicht nur Musik abspielt, sondern permanent lauscht und auf Zuruf Fragen beantwortet, die Todo-Liste ergänzt und mehr.

Die knapp 24 cm hohe schwarze Röhre mit einem Durchmesser von 8,3 cm „Amazon Echo“ ist einerseits ein über Bluetooth und WLAN verbundener Netzwerklautsprecher, der sich von Smartphone oder Tablet mit Musik von iTunes, Pandora und Spotify beschicken lässt. Andererseits wartet der mit Fernfeldmikrofonen und Spracherkennung ausgerüstete Echo auf Sprachkommandos. Dabei betont Amazon in dem Werbespot, dass man Echo nicht anbrüllen muss, sondern „überall im Raum gehört“ wird. Wie Apples „Siri“ und Googles „Ok, Google“ aktiviert ein offenbar wählbares Keyword – im Video „Alexa“ – den integrierten Personal Assistant. Alternativ soll man den Echo offenbar mit der dem Amazon Fire TV beiliegenden Voice Remote mit Mikrofontaste steuern können.

Laut Amazon gibt Echo Auskunft über das Wetter, buchstabiert Wörter, stellt den Wecker, spielt die Lieblingsmusik, rezitiert Wikipedia-Einträge, fügt der Einkaufsliste Einträge hinzu und so weiter. Das „Hirn“ von Echo sind die Amazon Web Services, über die ständig neue Kommandos ergänzt werden sollen.

Hochwertige Bass-Lautsprecher (2,5 Zoll) mit Bassreflex und Hochtöner (2 Zoll) versprechen klaren und verzerrungsfreien omnidirektionalen Klang. Über die Sprachsteuerung sollen sich Amazon (Prime) Music, iHeartRadio und TuneIn steuern lassen, während Musik von Spotify, iTunes und Pandora nur über Bluetooth von Mobilgeräten aus übertragen werden.

Amazon Echo gibt es vorerst nur in den USA zum Preis von 199 US-Dollar; Prime-Kunden müssen nur 99 US-Dollar bezahlen. Noch kann aber nicht jeder Echo kaufen. Interessenten müssen sich bewerben und bekommen eine Mail von Amazon, falls das Los auf sie fällt.

Fans von „Star Trek: The Next Generation“ („Computer … !?) werden ihre Freude an dem Gerät haben, wenn Echo das verspricht, was der Werbeclip von Amazon suggeriert. Auf Privatsphäre bedachte Naturen werden hingegen einen großen Bogen um den Lautsprecher machen und keinesfalls eine Amazon-Wanze im Wohnzimmer dulden – Microsoft kann ein Lied davon singen, man erinnere sich an das Horch und Guck der Xbox One. Ob es da hilft, dass Echo einen Schalter zum Deaktivieren des Mikrofon-Arrays besitzt, ist fraglich.

Doch was bezweckt Amazon mit dem Echo? Es wird ja kaum darum gehen, Eric Schmidt bloß zu beweisen, dass Amazon tatsächlich Googles größter Konkurrent ist. Sollte es wie beim Kindle (Fire) oder Fire TV (Stick) vor allem darum gehen, Amazons Inhalte besser an die Kunden zu bringen – also Bücher, Videos und Musik? Wohl kaum. Im Endeffekt dürfte es darum gehen, den Nutzern den perfekten Shopping-Assistenten an die Seite zu stellen, der die ausgesprochenen Wünsche direkt in dem Amazon-Einkaufskorb platziert …

Das liegt wohl an den grundverschiedenen Voraussetzungen. Star Trek

spielt aus menschlicher Sicht in einer Zukunft, in der die Existenz

des Individuums (zumindest der Spezies Mensch) ganz

selbstverständlich durch die allgemeinverfügbare Technik gesichert

ist. An der Stelle läßt sich die Technik wirklich nur noch gemäß der

Überzeugung der Spackeria (die sind seit NSA auch recht still

geworden) im Rahmen von Peinlichkeit gegen andere einsetzen. Heute

geht es dagegen darum, das Individuum bis an die Grenze der

(ökonomischen) Existenzfähigkeit auszupressen – und manchmal auch

darüber hinaus! (Source: http://www.heise.de/newsticker/foren/S-Re-Reaktion-der-Science-Fiction-Fans/forum-287951/msg-26049853/read/)

Die Zeichen dafür, dass sich das kapitalistische Nirwana nähert, mehren sich. Florian Stahl sieht sie überall. Beim Einkauf im Netz, in den USA, in Deutschland. Beispielsweise kürzlich in New York, als sich der Professor für quantitatives Marketing an der Universität Mannheim bei Booking ausloggte, die Cookies löschte, dann seine Hotelanfrage noch einmal startete, diesmal anonym. Da war das gleiche Zimmer plötzlich günstiger. Weil der Algorithmus ihn nicht mehr identifizieren konnte, schlug er ihm einen anderen Preis vor. „Die Preismechanismen sind dabei, sich zu ändern“, sagt Stahl, „und zwar fundamental“.

Im Prenzlauer Berg, im Kaiser’s Supermarkt in der Winsstraße, wo sich Berlin früher zum Flirten traf, drängen sich die Kunden vor einem roten Ständer mit einem Bildschirm. Sie halten eine Karte vor den mannshohen Apparat. Weißes Licht streichelt ihre Hände, ihre Extrakarte wird gescannt, ein leises Summen begleitet das Erscheinen des Bons, darauf ihre Preisabschläge. Dann bin ich dran.

Ich checke ein in die Beta-Phase der dritten industriellen Revolution. Bald soll mich der Kaiser’s Algorithmus komplett verstehen, meine Wünsche vorhersagen können, noch aber kennt er mich nicht. Er hat bisher keinen einzigen Kassenzettel von mir gescannt, nur meine neue Extrakarte. Es ist ein Riesenerfolg in der Kundenkarten-Welt: Ein Drittel der Stammkäufer wurde in den ersten zwei Monaten seit der Einführung Nutzer. Mein Ausdruck zeigt „Ihre persönlichen Angebote heute“: Je 20 Prozent Abschlag für Harry Brot (noch nie gehört) und Bärenmarke Alpenfrische Vollmilch (dachte, die machen nur Kaffeesahne); für Barilla Nudeln gibt es 30 Prozent, für Ritter Sport und Lätta Margarine sogar 40.

Vor gut hundert Jahren beobachtete Arthur Cecile Pigou, Professor in Cambridge, ein seltsames Phänomen: Er sah ins Herz des Kapitalismus und es war leer. Der Preis, um den sich die Marktwirtschaft als System der freien Preise dreht, existierte in Wahrheit gar nicht. In The Economics of Welfare von 1920 beschrieb Pigou seine Beobachtung im Kapitel Das spezielle Problem der Eisenbahntarife: Für eine identische Leistung, die gleiche Bahnfahrt von A nach B, zahlten Menschen freiwillig verschiedene Tarife, je nach Klasse. Pigou erkannte, was für die Ökonomie heute so elementar ist wie die Unschärferelation für die Physik: Es gibt keinen objektiv richtigen Preis einer Ware. Es gibt einzig persönliche Werteinschätzungen.

„Preisdiskriminierung“ nannte Pigou die Unterscheidung von Menschen nach den Preisen, die sie für das gleiche Produkt zu zahlen bereit sind. Für Händler ist sie eine wunderbare Möglichkeit, mehr für die gleiche Leistung zu kassieren. In der Vollendung der Preisdiskriminierung, der „Preisdiskriminierung ersten Grades“ könnten Anbieter, so Pigou, jedem einzelnen Käufer einen Höchstpreis für die Bahnfahrt setzen – und ihm so alles abnehmen, was er überhaupt zu zahlen bereit ist. Fortan lernte jeder Ökonomiestudent die totale Preisdiskriminierung als den heiligen Gral des Kapitalismus kennen.

An der Kaiser’s Kasse zeige ich die Extrakarte, piep!, registriert. Jeder Kauf verändert meine zukünftigen Preise: Ladenpreis minus persönlicher Rabatt. Erst einmal bin ich auf keines der Angebote eingegangen, weder Lätta noch Ritter Sport. Am Scanner hole ich mir den nächsten Bon. Wieder das gleiche Angebot. Dreimal muss ich da durch. Dann ist der Algorithmus angeblich soweit.

Personalisierte Angebote als letzte Möglichkeit, den Umsatz zu steigern

Fixe Preise schaffen einen versteckten Sozialvertrag, wie einheitliche Krankenkassenprämien. Hinter Einheitspreisen in Supermärkten, Bahnhöfen und Drogerien steckt ein Gesellschaftskonzept: Alle Käufer sollen gleich sein.

Einheitspreise schaffen Gewinner und Verlierer – dem einen ist etwas eigentlich mehr wert, dem nächsten ist es fast zu teuer. So subventionieren wir einander, vom Joghurtkauf bis zur Taxifahrt. Am meisten profitiert der Durchschnittsmensch. Im Massenmarkt seien personalisierte Preise bislang technisch unmöglich, sagt Florian Stahl, weil sie das Wissen über die Wertschätzung des Käufers für ein bestimmtes Produkt zu einem bestimmten Moment voraussetzten. In diese Wertschätzung könne theoretisch alles einfließen, bis hin zur Wetterlage, wie bei Eis oder Jacken. „Den individuellen Höchstpreis zu erkennen, ist eigentlich ein unendliches Problem“, sagt Stahl.

Lange entsprachen Preise im Alltag dem geschätzten Wert dessen, was unterschiedliche Käufer im Schnitt zu zahlen bereit waren. Bis die Computer kamen, das Internet, Facebook, Google, Scanner, Produkt-IDs, In-Store-Cams, Smartphones – ein Arsenal zur Datafizierung von Personen, deren Vorlieben, Verwandtschaftsverhältnissen, Jobs, Bewegungsmustern, Wertvorstellungen. Seit Kurzem gibt es nun Algorithmen, die die Daten zu dynamischen, individuellen Preisen zusammenrechnen können, wie zuerst die Flugpreise, dann die Hotelpreise, die Elektrizitätspreise und so weiter. Jetzt deutet sich an, dass sich alles herunterbrechen lässt auf den Einzelnen. Es ist, als ob ein Märchen wahr würde.

Das Klingelschild ist golden, Oderberger Straße 44, beste Lage im Prenzlauer Berg, direkt neben dem Modeladen Kauf Dich Glücklich. SO1 steht an der Klingel, kurz für Segment of One. Während in den USA mehr als die Hälfte aller Handelsunternehmen mit sogenannten Price Intelligence Verfahren und dynamischen Preisen experimentiert, jeder zwanzigste Preis bereits personalisiert ist, während die Preisschilder in Frankreich zunehmend durch Digitalanzeigen ersetzt werden, ist das Berliner Start-up SO1 einer der ersten deutschen Anbieter für totale Preisdiskriminierung.

Hier arbeiten 15 Statistiker, ITler, Ökonomen. Menschen, die Google und Henkel verlassen haben, um eine Vision Wirklichkeit werden zu lassen. Sie stecken hinter den roten Automaten in derzeit 30 Berliner Kaiser’s Testmärkten. Die Extrakarte sei eigentlich wie ein physischer Cookie, erklärt der junge Chef und Mitgründer Raimund Bau. SO1 trage die absolute Preisdifferenzierung aus dem Netz, wo Amazon oder Zalando längst so arbeiteten, in die Welt. Die Karten hätten eine anonyme Kundennummer, man brauche im Gegensatz zu anderen Kundenkarten keine persönlichen Informationen wie Namen oder Adresse. Darauf ist Bau stolz. Erfasst würden an der Kasse nur Kaufzeit, Produktnummer, Kartennummer und der gezahlte Preis. „Bei uns laufen die Daten aus den Kassen zusammen. Wir können beispielsweise identifizieren, wer ein Pepsikäufer ist, sogar wenn er nie Pepsi bei Kaiser’s gekauft hat.“ Das ergebe sich allein aus der erfassten Kombination gekaufter Produkte. Jedes Produkt sei ein statistischer Hinweis auf andere Produktvorlieben, so wie Weleda-Shampoo auf Bio-Obst hinweist.

Auf Basis der Wahrscheinlichkeiten, die aus Testmärkten bekannt seien, könnten nicht nur Vorlieben errechnet werden, so Bau, sondern auch die persönliche Zahlungsbereitschaft und Preissensibilität. „Wenn wir den Cola-Absatz erhöhen wollen, finden wir heraus, ob Du als Pepsi-Liebhaber für Cola ein potenzieller Kunde bist. Ob Du es wiederholt kaufen würdest, wenn Du es einmal ausprobierst. Wie viel wir Dir zahlen müssten, um Dich zum Cola-Kauf zu bringen.“ Lohne sich der Kunde für Cola, biete man ihm an den roten Automaten genau den passenden Preisnachlass für Cola. Resultat seien individuelle Preise.

Der gläserne Kunde

Heute arbeite SO1 noch mit Bons, bald werde vieles über Apps laufen, sagt Bau. „PayPal, Mastercard, Google arbeiten sicherlich an ähnlichen Methoden.“ Absolute Preisdiskriminierung sei eine weltweite Bewegung, die kaum aufzuhalten sei, weil in gesättigten Märkten wie dem Lebensmittelhandel der Preiswettkampf der einzige Weg sei, den Umsatz zu steigern. „Persil wäscht jetzt noch weißer“ ziehe nicht mehr, sagt Bau. Und altbekannte Promotionen via Coupons oder Rabattmarken hätten aufgrund der Streuung kaum Effekt. Sie würden vor allem von Leuten genutzt, die das Produkt sowieso kaufen würden. Die Extrakarte bringe dagegen pro Nutzer Umsatzsteigerungen im mittleren zweistelligen Prozentbereich. Für Bau eine Win-Win-Win-Win-Situation für Kunde, Händler, Produzent und SO1.

Das will sich auch IBM nicht entgehen lassen. Demandtec heißt die Software des Konzerns. Große Ketten, Lebensmittelhändler, Drogerien oder Baumärkte sollen sie nutzen, um ihre Preise auf Basis von persönlichen Kaufmustern, Konkurrenzpreisen oder anderen Einflüssen ständig zu optimieren. Das ermöglicht verschiedene Preise von Supermarkt zum Onlineshop zum Mobilgerät oder zwischen Gebieten. Eine zweite IBM-Software namens Xtify bietet Techniken, um Kunden jederzeit ortsbezogen mit Angeboten anzusprechen.

Alle Informationen werden zusammengenommen

Viele Geschäfte haben sich derweil zu veritablen Überwachungsdiensten entwickelt. Das Ziel: Kunden bis ins Detail ausforschen. In der Schweiz können die beiden führenden Supermarktketten Migros und Coop 80 Prozent aller Einkäufe Haushalten zuordnen, dank der Kundenkarten. Niemand weiß mehr über die Schweizer, über ihre Allergien, Aufenthaltsorte, Gewohnheiten, Familienstrukturen, Adressen. Bei der US-Kette Safeways nutzt fast die Hälfte aller Kunden eine App, die ihnen im Supermarkt spezifische Nachlässe anzeigt, beruhend auf der eigenen Shoppingvergangenheit. So entstehen personalisierte Preise.

Ich habe Harry Brot und Barilla Nudeln verbilligt gekauft. Die beiden Angebote fehlen jetzt auf dem dritten Ausdruck. Sonst ist alles beim Alten. Noch ein Einkauf, dann kann ich sehen, was der Kaiser’s Algorithmus von mir denkt. Ob er mir Cola anbietet?

„Von der Ernährung über die Mobilität bis zur Energieversorgung sind elementare Bereiche unseres Lebens von den neuen Preismodellen betroffen“, sagt der St. Galler Ökonom und Zukunftsforscher Joël Cachelin. Und diese Preise würden durch uns unbekannte und unüberprüfbare Kriterien bestimmt.

Alles wird verknüpft

Die für den Einzelnen bedrohlichste Möglichkeit wäre künftig die Verknüpfung aller Informationen über Firmen und Netzwerke hinweg. Jede unserer Handlungen und Äußerungen, auch vergangene, würde den Preis beeinflussen, den wir für etwas zahlen. Das Netz würde zu einer Art Credit History, wie Kritiker des neuen Facebook Werbedienstes Atlas befürchten.

In Dänemark bietet der Reiseveranstalter Spies derzeit schon Sonderpreise für Paare an, die in ihren Ferien nachweislich ein Kind zeugen. Der Werbegag ist ein Versuch, mit Preisen einem der größten Probleme Dänemarks zu begegnen: dem Mangel an Nachwuchs. Preise sind eines der wichtigsten Steuerungsmittel unserer Gesellschaft. Sie sind Politik. „Die Zeiten des Sozialvertrags im Preis gehen zu Ende“, sagt Florian Stahl. Zukünftig könnten Menschen sogar Identitäten tauschen, um niedrigere Preise zu zahlen.

Brotpreise starten Revolutionen. Was aber passiert mit einer Gesellschaft, deren Preissystem sich komplett ändert?

Nach dem dritten Einkauf gehe ich zum Automaten, um endlich mein persönliches Angebot zu erhalten. Das Licht des Scanners wärmt meine Hand. Mein Rabatt erscheint mit sanftem Summen. 20 Prozent auf Bärenmarke Milch, 40 Prozent auf Lätta Margarine.

Amazon erfindet den Lauschsprecher

Amazon Echo: Eine Dystopie in Zylinderform.

Die Gebrauchsanweisung für Amazons neues Produkt hat in ihrer deutschen Ausgabe 351 Seiten und erzählt nebenbei noch die Geschichte einer totalitären Diktatur. Es ist das Buch „1984“ von George Orwell – und das wichtigste Instrument in dieser Dystopie ist der Televisor, der bei allen Bürgern zu Hause fest installiert ist. Er hört alles, kann sprechen und dient auch als Fernseher.

Einen kleinen Unterschied gibt es allerdings: Ein Fernseher ist Amazons „Echo“ nicht und es bleibt auch jedem selbst überlassen, ob er die kleine, schicke, schwarze Säule bei sich zu Hause aufstellt, wo sie fortan auf Sprachkommando reagiert und ihrem Besitzer Fragen beantwortet. Wie zum Beispiel: Alexa, wie viel Uhr ist es? Alexa, wie buchstabiert man Mountainbike? Alexa, wie kocht man Bolognese? Das Codewort Alexa aktiviert Echo.

Das Gerät kann all das, weil es permanent mit dem Netz verbunden ist – und weil Echo offenbar alles hört, was um die kleine Säule herum gesprochen wird. Kein Hersteller hatte bislang die Chuzpe, dieses Gerät wirklich zu bauen und anzubieten. Amazon, der Lieferkonzern, hat die Chuzpe, unsere Gesellschaft zu verändern. Wenig innovative Buchhandlungen und Verlage zu ruinieren. Unseren Konsum zu protokollieren. Produkte will der Konzern seinen Kunden künftig per Drohne liefern – Amazon weiß schon, was gut für uns ist. Dieser Konzern also hat den Televisor gebaut. Herzlichen Glückwunsch!

Die Standleitung zu einem Amazon-Server

Und warum auch nicht. Die gesamte Umgebung um uns herum sammelt Daten. Unsere Handys sowieso, unsere Autos, Bankautomaten, Kassen, Kameras, öffentliche wie private, Payback-Karten, Webseiten, die wir besuchen. Dass Echo da so heraussticht, liegt an zwei Aspekten. Erstens: Echo soll im Wohn- und Schlafzimmer stehen. Das Gerät überwacht – oder bereichert – unser zu Hause. Zweitens: Echo ist, wie man es von Amazon kennt und erwartet, ein besonders innovatives Produkt. Es ist ein Wagnis, aber eines das sich lohnen könnte. Echo rückt uns dort näher ans Netz, wo wir bislang konsequent offline sind. Im Wohnzimmer, beim Faulenzen, beim Kochen, beim Schlafen, im Bett. Echo ist, einem Handy nicht unähnlich, die Standleitung unseres Lebens zu einem Amazon-Server. 199 Dollar kostet das Gerät in den USA, bislang können nicht alle Kunden bestellen, Amazon testet noch, wie das neue, ungewohnte Gerät angenommen wird.

Vielleicht hat Amazon deshalb einen betont konservativen Werbespot zu Echo gedreht, der vor allem suggeriert: Echo macht das Leben einfacher. Ansonsten bleibt alles, wie es ist. Vati hört die Nachrichten mit Echo, Mutti kann den neuen Mitbewohner erst nicht richtig bedienen, aber rafft es dann doch noch – so einfach ist Echo! – und kann in Ruhe mit Echos Hilfe kochen. Und es stimmt ja auch: Nicht das Gerät ist das größte Problem, sondern die fehlenden Regeln für das Gerät. Der Zwang, dem Kunden transparent zu zeigen, was mit ihm geschieht, wenn er das Gerät verwendet. Echo ist nämlich nur die Vorderseite des Produktes, das man erwirbt. Den schwarzen Zylinder kann man anfassen, aber für den Kunden nicht greifbar ist der Amazon-Webserver, der mit Echo verbunden ist und der mit jedem Wort, das in Echos Hörweite fällt, dazu lernt. Über den Sprechenden. Über seinen Tonfall, seine Stimmung, seine Wünsche, seine Probleme, seine Hoffnungen, sein Leben.

Daten, die besonders wertvoll sind

Echo sammelt jene Kategorie von Daten, die besonders wertvoll und besonders kritisch ist, nämlich personenbezogene Daten. Und der Service wäre nicht halb so bedenklich, wenn er klar geregelt wäre und für den Nutzer vollkommen transparent wäre, wie und wo seine Daten liegen, wer sie bekommt und was mit ihnen angestellt wird. Aber welchen Gesetzen gehorcht Echo überhaupt? Amerikanischen? Deutschen? Wer hat Zugriff auf die Daten? Was geschieht mit den Profilen, die unweigerlich entstehen, wenn Echo immer lauscht?

Amazon in Deutschland konnte eine entsprechende Anfrage der Süddeutschen Zeitung nicht beantworten und verweist auf die amerikanische Pressestelle, die bislang nicht reagiert hat. Auf der Echo Produktseite, auf der sich bislang nur amerikanische Nutzer um ein Gerät bewerben können, sind die Vorteile von Echo ausführlich erklärt. Der tolle Klang der Lautsprecher, wie genau Echo höre, was gesprochen wird, wie sich Echo mit anderen Geräten verbinden lässt. Der Hinweis zum Datenschutz aber führt nur zur ganz gewöhnlichen Amazon.com-Datenschutzseite, die Allgemeinplätze und Standardtexte für den Nutzer bereithält. Wer Echo besitzt, weiß deshalb tatsächlich nicht, wie ihm geschieht. Vielleicht ist es nochmal an der Zeit, die 351 Seiten der inoffiziellen Gebrauchsanweisung zu lesen.

An increasingly bigger box. (Reuters/Rick Wilking)

Amazon has a tendency to polarize people. On one hand, there is the ruthless, relentless, ferociously efficient company that’s building the Sears Roebuck of the 21st century. But on the other, there is the fact that almost 20 years after it was launched, it has yet to report a meaningful profit. This chart captures the contradiction pretty well—massive revenue growth, no profits, or so it would seem. But actually, neither of these lines gives you a good sense of what’s really going on.

Amazon discloses revenue in three segments—Media, Electronics & General Merchandise (‘EGM’) and ‘Other’, which is mostly AWS. As this chart shows, these look very different (this and most of the following ones use ’TTM’—trailing 12 months, which smooths out the seasonal fluctuations and makes it easier to see the underlying trends). The media business is still growing, but it’s the general merchandise that has powered the explosion in revenue in the past few years. Meanwhile, the ‘Other’ line is growing but is still much smaller.

Splitting out the detail, we can see this trend both in North America (NA) and internationally…

Though the takeoff is particularly strong in the USA.

Media overall was only 25% of Amazon’s revenue last quarter, and 20% of North America.

And if we go back to ‘Other’ and zoom in, the growth is pretty dramatic there too.

It seems pretty likely that these businesses, selling very different products bought with different bargaining positions to different people with different shipping costs, have different margin potential.

This still doesn’t really give an accurate picture, though. Amazon is in fact organized not just in these segments, but in dozens and dozens of separate teams, each with their own internal P&L and a high degree of autonomy. So, say, shoes in Germany, electronics in France or makeup in the USA are all different teams. Each of these businesses, incidentally, sets its own prices. Meanwhile, all of these businesses are at different stages of maturity. Some are relatively old, and well established, and growing slower, and are profitable. Others are new startups building their business and losing money as they do so, like any other new business. Some are very profitable, and some sell at cost or at as loss-leaders to drive traffic and loyalty to the site. Books are a good example. There’s a widespread perception that Amazon sells books at a loss, but the average sales price actually seems to be very close to physical retailers—it discounts some books, but not all, and despite all the argument in the Agency lawsuits, quite how many and how much is (deliberately) as clear as mud.

Amazon is a bundle.

The clearest expression of this is Prime, in which (amongst other things) entertainment content is included at a high fixed cost to Amazon (buying the rights) but no marginal cost beyond bandwidth, as a way to enhance the appeal of being a Prime ‘member’. Prime membership in turn draws people to switch more and more of their online and offline spending to Amazon. Trying to look at the profitability of the video alone misses the point.

And then there are the third party sales. Just as AWS is a platform both for Amazon’s own internal technologies and for thousands of startups, so too the logistics and commerce infrastructure themselves are a platform for lots and lots of different Amazon businesses, and also for lots of other companies selling physical products through Amazon’s site. Third party sales of products through Amazon’s own platform are now 40% of unit sales, and the fees charged to these vendors are now 20% of Amazon’s revenue.

This means, in passing, that for close to half of the units sold on Amazon.com, Amazon does not set the price, it just takes a margin. This alone should point to the weakness of the idea that Amazon’s growth is based on selling at cost or at a loss.

The tricky thing about these third party (‘3P’) sales is that Amazon only recognizes revenue from the services it provides to those companies, not the value of the goods sold. So if you buy a pair of shoes on Amazon from a third party, Amazon might collect payment through your Amazon account and ship them from its warehouse using its shipping partners—but only show the shipping and payment fees it charged to the shoe vendor as revenue. It does not disclose the gross revenue (‘GMV’). Given that (as it does disclose) third party sales tend to have a higher unit value, this means that the total value of goods that pass though Amazon with Amazon taking a percentage is perhaps double the revenue that Amazon actually reports. So, the revenue line is not really telling you what’s going on, and this is also one reason why gross margin is pretty misleading too. Gross profit has risen from 22.4% in 2011 to 27.2% in 2013, but this does not really reflect a change in consumer pricing and margins thereof, but rather this change in mix.

So, we have dozens of separate businesses within Amazon, and over two million third party seller accounts, all sitting on top of the Amazon fulfillment and commerce platform. Some of them are mature and profitable, and some are not. And someone at Amazon has the job of making sure that each quarter, this nets out to as close to zero as possible, at least as far as net income goes. That is, the problem with net income is that all it tells us is that every quarter, Amazon spends whatever’s left over to get the number to zero or thereabouts. There’s really no other way to achieve that sort of consistency.

If you listen closely, Amazon itself tells us this. The image below comes straight from Amazon—originally it was a napkin sketch by Jeff Bezos. Note that there’s no arrow pointing outwards labeled ‘take profits.’ This is a closed loop.

(Source: Amazon)

In any case, profits as reported in the net income line are a pretty bad way to try to understand a business like this—actual cash flow is better. As the saying goes, profit is opinion but cash is a fact, and Amazon itself talks about cash flow, not net income (Enron, for obvious and nefarious reasons, was the other way around). Amazon focuses very much on free cash flow (FCF), but it’s very useful to look also at operating cash flow (OCF), which is simply what you get adding back capital expenditure (‘capex’). In effect, OCF is the bulk of running the business before the costs of the infrastructure, M&A and financing costs. This shows you the effect of selling at low prices. As we can see here, Amazon’s OCF margin has been very roughly stable for a decade, but the FCF has fallen, due to radically increased capex.

In absolute terms, you can therefore see a business that is spinning out rapidly growing amounts of operating cash flow—over $5bn in the last 12 months—and ploughing it back into the business as capex.

Charting this as lines rather than areas shows just how consistent the growth in capex has been.

One might suggest that in a logistics business with rapid revenue growth, rapid capex growth is only natural, and one should look at the ratio of capex to sales by itself. But in fact, the increase here is even more dramatic. Starting in 2009, Amazon began spending far more on capex for every dollar that comes in the door, and there’s no sign of the rate of increase slowing down.

If Amazon had held capex/sales at the same ratio from 2009, before it exploded, then FCF would look like this. That difference adds up to just over $3bn of cash in the last 12 months. That is, if Amazon was spending the same on capex per dollar of revenue as it was in 2009, it would have kept $3bn more in cash in the last 12 months.

So where’s all the extra capex going? And, crucially, does it need to stay at these new, higher levels to support Amazon’s business, or can it come back down in the future?

It’s pretty apparent that the money is going into more fulfillment capacity (warehouses, to put it crudely) and to AWS. Hence, this chart shows an enormous increase in Amazon’s physical infrastructure, as measured in square feet—this is almost all fulfillment rather than data centers, though Amazon no longer gives a split.

Pulling apart precisely where the money’s going, though, is a little fiddlier. The increase is driven by some combination of four things:

More capacity for more products, including 3P products

Proximity—as Amazon builds warehouses closer to customers, the shipping time goes down and so too does the shipping cost, a further flywheel effect for Prime

AWS

More expensive warehouses—that is, the existing business is becoming more expensive to run

The first two of these are straightforward investment in the future, often delivering higher future margins. AWS is a black box and a much debated puzzle, but it is also pretty much the definition of a new business that requires investment to grow. The real bear case here would be the last point— that the existing business is becoming more capex-intensive—that more dollars of capex are needed for every dollar of current revenue.

Just to make life harder for those looking to understand Amazon’s financials, the warehouse expansion, capex expansion and AWS build-out all started at roughly the same time, and at that same moment Amazon changed the way it reports to make it very hard to pick them apart. Until 2010 it split both property and asset value between fulfillment and data centers, but at that point it stopped, probably not by coincidence (in 2010 Amazon had just 775,000 square feet for data centers and customer service combined). In the meantime, there are various metrics (capex per square foot, for example) that would show a shift of spending from cheap warehouse to expensive data centers—but they would also show a shift from maintaining existing warehouses to building new ones. So there is no direct, easy way we can see the split.

We can still, though, get a something of a sense of the key warehouse question—has the business gotten more expensive to run? It looks like the answer is no. First, the third party sales do not seem to be the issue: ratio of 3P units has not gone up at anything like the way the capex/sales has over the same period (here’s that chart again).

Neither is there any sign of a shift in the fulfillment costs over the period (Amazon seems to have forgotten to stop disclosing these). The physical product mix hasn’t got dramatically more expensive to ship, so would it get dramatically more capex-intensive to warehouse? This is obviously not an exact proxy, but it seems unlikely.

So, though we can’t be sure, it looks like the capex is not going up because Amazon’s existing business has become more expensive to run, but because Amazon is investing the growing pool of operation cash flow into the future. All of this brings us back to the beginning—Amazon’s business is delivering very rapid revenue growth but not accumulating any surplus cash or profits, because every penny of cash is being ploughed back into expanding the business further. But, this is not because any given business runs permanently at a loss—it is because the profits from what is already there are spent on making new businesses. In the past, that was mostly in operations, but in recent years the investment firehose has again been pointed at capex.

How long will this investment go on for? Well, do we believe that the conversion of products and businesses to online commerce is finished? Let’s rebase that revenue chart, and look at it as share of US retail revenue. Excluding gasoline, food and things like timber and plants, all hard to ship, at least for now, Amazon has about 1%.

Overall, US commerce is growing very consistently:

And Amazon is taking an accelerating share of it.

Amazon has perhaps 1% of the US retail market by value. Should it stop entering new categories and markets and instead take profit, and by extension leave those segments and markets for other companies? Or should it keep investing to sweep them into the platform? Jeff Bezos’s view is pretty clear: keep investing, because to take profit out of the business would be to waste the opportunity. He seems very happy to keep seizing new opportunities, creating new businesses, and using every last penny to do it.

Still, investors put their money into companies, Amazon and any other, with the expectation that at some point they will get cash out. With Amazon, Bezos is deferring that profit-producing, investor-rewarding day almost indefinitely into the future. This prompts the suggestion that Amazon is the world’s biggest ‘lifestyle business’—Bezos is running it for fun, not to deliver economic returns to shareholders, at least not any time soon.

But while he certainly does seem to be having fun, he is also building a company, with all the cash he can get his hands on, to capture a larger and larger share of the future of commerce. When you buy Amazon stock (the main currency with which Amazon employees are paid, incidentally), you are buying a bet that he can convert a huge portion of all commerce to flow through the Amazon machine. The question to ask isn’t whether Amazon is some profitless ponzi scheme, but whether you believe Bezos can capture the future. That, and how long are you willing to wait?

The recent run-up in Amazon.com’s (NASDAQ:AMZN) stock price inspired me to revisit an old thorn in my side. AMZN is up 12.2% since the beginning of 2013, despite a very tough retail sales environment and despite the fact that California and some other states now collect what is known as „the Amazon tax.“ In addition, a bill to collect a Federal Internet sales tax was reintroduced in Congress two weeks ago: Online sales tax.

With this in mind, I decided to peruse AMZN’s 2012 10-K, something I had not done in years, to see what was going beneath the headline „veneer“ applied heavily to AMZN’s quarterly sales and net income results.

I knew that AMZN was using some controversial accounting methodologies, but when I pulled apart the financial statements and applied some old fashioned financial analysis, what I found with regard to AMZN’s cost structure, cash flow and true profitability was quite shocking. Looking at some income statements, cash flow from operations and balance sheet indicators, some of which Wall Street never discusses – AMZN looks somewhat like a Ponzi scheme. I say this because I believe it is likely that a serious cash problem for AMZN will develop if its sales growth slows down or even goes flat.

Let’s look at some numbers I put together by „pulling apart“ AMZN’s financial statements from its 2012 10-K (linked for your convenience). I created the table below to focus on what I consider to be the key metrics in understanding the true ability of AMZN’s business model to generate meaningful cash flow. Standard GAAP/adjusted-GAAP accounting statements often use accounting gimmicks that mask true profitability, which I’ll demonstrate below:

First, I wanted to look at cash flow generated by operations. This number is a fairly „clean“ indicator of how profitable the business model is, as it adjusts the reported income for all non-cash charges, adjusts for any non-operating gains/losses and reflects cash required to finance receivables and make vendor financing payments. As you can see, despite robust sales growth over the last three years, the cash generated by each additional dollar of sales is decreasing rapidly, as reflected by the trend shown in line (1) above. While it’s true that a smaller percentage of a growing sales number is still an increase, you can see that from 2011 to 2012 sales jumped by $13 billion but operational cash flow only increased by $271 million. This is a red flag. Please note, this cash flow number does not include AMZN’s big capex program – it’s purely a measure of AMZN’s organic operational profitability

Second, I believe a big part of the declining cash flow margin comes from AMZN’s cost of fulfillment – the cost delivering products to the end-buyer. I have always believed that AMZN’s business model generated tremendous sales growth because AMZN’s fulfillment strategy, in effect, heavily „subsidizes“ the all-in price paid by the customer. As you can see in (2) above, AMZN’s fulfillment costs have increased as a percent of its cost of goods sold in each of the last three years.

In fact, the way AMZN accounts for fulfillment is quite controversial: AMZN’s accounting. AMZN does not include fulfillment costs in its cost of goods sold (COGS), despite the fact that shipping – getting sold products to the buyer – is an integral part of the all-in cost of products sold in AMZN’s business model/strategy. AMZN’s „holy grail“ is that it can sell products over the Internet more profitably than „brick and mortar“ retailers, so the cost of delivery should be part of the cost of sales.

It’s a grey area of FASB rules, but not including this expense in the COGS distorts AMZN’s gross margins vs. that of competitors. (2) in the table above shows AMZN’s gross margin with and without fulfillment costs. As you can see from the difference in the two metrics, AMZN is heavily incentivized to keep the cost of fulfillment out of its COGS calculation. Gross margin is a key metric for analyzing profitability. In 2012, Target’s (NYSE:TGT) gross margin was 31%, Wal-Mart’s (NYSE:WMT) was 25% and Best Buy’s (NYSE:BBY) was 24.6%. You can see why AMZN has refused to consider fulfillment costs as part of the cost of a product, despite the fact that it is a key component in generating revenue. Fulfillment costs have been a rising part of AMZN’s overall product cost. As the cost of energy, and there the cost of shipping, increases it will put even more of a squeeze on the cash margin AMZN earns with each sale.

Third, AMZN’s operating margin is razor thin compared to its comparables. You can see from (3) in the table above that it’s been deteriorating quickly over the last three years. For 2012, TGT and WMT had operating margins of 7.6% and 5.6%, respectively. Remember, AMZN’s theory with its business model is that it can operate less expensively than its „brick and mortar“ rivals. The numbers for the last three years suggest that AMZN fails to deliver on this.

Let’s now look a little more deeply at the cash being generated by AMZN’s operations and why I believe AMZN resembles more of a Ponzi scheme than people realize. In addition to cash being generated by sales, „cash provided by operations“ also includes changes in working capital. Inventory is a use of cash; accounts receivable, accounts payable and other current liability accruals are sources of cash.

Retailers tend to have a much larger amount of accounts payable than they do receivables. Cash comes immediately from sales and companies negotiate payment terms from vendors, etc, thereby giving retailers the „float“ on cash generated by operations. In order for this model to work, it is important for sales to grow over time, as the „velocity“ of „cash in“ needs to stay ahead of the velocity of „cash out,“ otherwise a liquidity problem can develop.

I chose to isolate and focus on AMZN’s accrued expenses because the payables have been increasing at a normal rate. However, the accrued expense account (3) has been increasingly a significant portion of AMZN’s „cash provided by operations,“ – its „cash in.“ As you can see from the table above, accrued expenses are growing and have gone from just 17% of cash flow from operations to over 47%. This is a big red flag.

Accrued expenses are largely cash from the sale of gift cards. If gift cards go unused, and some do, they accrue 100% to operating income. AMZN doesn’t disclose the other sources of accrued expenses, but it isolates „unearned revenues“ in its cash flow statement (4) – this is gift card cash. As you can see, gift card sales have been a growing source of cash funding over the last three years, representing 43% of cash generated by operations in 2012. If I didn’t know exactly what business AMZN was in, I would be under the impression that it was trying to become a gift card sales operation.

My point here is that – at 43% of cash generated by operations – AMZN is become increasingly reliant on the „float“ it gets from gift cards in order to fund its operations on a short term basis. If AMZN’s revenues slow down or its expenses unexpectedly increase, for whatever reason, AMZN could face liquidity problems.

What happens if sales slow down because of a bad economy or predatory competitors? On Monday (March 3) Wal-Mart announced that it was going to start going after AMZN’s „Marketplace“ web vendor business: Wal-Mart/Amazon. This will likely „cannibalize“ AMZN’s „net service sales,“ which has gone from 10% of revenues to nearly 15% over the last three years. AMZN doesn’t break out its income from its revenue segments, but its Marketplace business is likely very high margin, meaning it’s become an important part of cash generated by operations. In addition, the imposition of the internet „Amazon tax“ will increase the customer’s all-in cost to buy from AMZN, which could significantly impact sales negatively.

AMZN’s market cap as of the 3/7/2013 close is $124.5 billion. Based on 2012 operating income, it’s trading at 185x operating income. For comparison purposes, WMT and TGT trade respectively at 9.2x and 8x their 2012 operating income. The p/e comparison is irrelevant because AMZN lost money on a net income basis in 2012, but that multiple of cash flow unequivocally represents an irrational „bubble“ valuation.

AMZN’s market cap has always been one of the unsolved mysteries of the stock market. Moreover, in its entire operating history, AMZN has never generated meaningful income or cash flow. It is clearly highly overvalued relative to its peers. But, I have rarely made money either shorting the stock or buying puts. It’s been a long-time source of frustration and at this point I’m going to wait until I see the signs that the Ponzi-like cash funding scheme AMZN has in place starts to deteriorate and then I’m going to pounce hard on the short side. Given that retail sales seem to be slowing down – and by some metrics declining – with the economy, and given that Wal-Mart is going to start throwing its weight around at one of AMZN’s key sources of cash flow, I don’t think I’ll have to wait much longer.

Every few months, headhunting firms and recruitment consultants release surveys about hiring trends in the country and in the recent past, every survey has something for the Non Resident Indian.

India today, offers better employment opportunities as compared to some of its global peers.

But while landing a job in itself might not be difficult, there are some sectors that are keenly looking out to hire those with global experience. “Some sectors require a certain level of skill and experience that are not available within India Companies in these sectors look at hiring from outside India. And if you are an NRI, with these sought after skills, you might just be the right person the company is looking for,” says Aseem Juneja, a cross border talent expert and founder of Indbound.com.

And while the salaries in India tend to be around 40-70% of dollar salaries, because these skills are much in demand, salaries can be much higher. Kris Lakshmikanth Founder CEO of The Head Hunters India Pvt Ltd.

Says, “Salaries could go up to 100% of dollar salaries in a lot of these cases.”

So which are these sectors? Let’s take a look.

1) HEALTHCARE

Healthcare here mainly includes biotechnology, contract research and manufacturing, clinical research and pharmaceutics.

According to this E&Y Report , the Indian biotechnology sector was valued at USD 4 billion in 2010 growing at nearly 21%, in value over 2000-2010. It is estimated that as of 2012, the Indian CRAMS sector (Contract Research and Manufacturing) will be valued at USD 7.6 billion growing at a CAGR of 47.2% from 2007 till 2012. Express Pharma envisaged that by 201 India would be conducting 15% of all global clinical trials.

“India is fast becoming a hub for outsourcing in the healthcare sector,” says Kris Lakshmikanth Founder CEO of The Head Hunters India Pvt Ltd, adding, “Multinational companies like Pfizer, Novartis, Eli Lilly etc look at India as a skilled and cost effective hub to outsource certain functions. This includes research in areas like stem cell and vaccinations, contract research and clinical re search. While the employees of these outfits are largely from within India, the leadership team of these units is typically those with global experience.”

“Typically, those with a post doctoral qualification with research experience in the US would fit the bill,” he says.

2) TELECOM

“The telecom sector in India has seen an explosive growth in subscriber base and volumes. However, margins in voice based service are thin and companies are looking beyond voice. They are looking at value added services (VAS) and the availability of high bandwidth, upgrades and rollouts of technologies (3G etc) is making that possible,” Juneja explains.

This report from PriceWaterhouse Coopers states: The mobile tariffs in India are one of the lowest in the world and due to hypercompetition in telecom it is not expected to rise in near future. VAS remains only effective tool to increase the ARPU/share of wallet of subscribers. Multilingual content, application support around languages, killer applications and readiness of handsets could drive over Rs 55,000 crore of VAS revenue by 2015.

With the launch of 3G services and expected launch of high bandwidth BWA services, VAS currently has reached its inflexion point.

The constituents of VAS ecosystem such as mobile operators, content creator, handset manufacturer will need to show greater collaboration to achieve full potential of VAS.

“Companies need people to build applications and bring innovative services to the table. And currently, much of these skill sets are only available in the developed markets like the US,” Juneja says.

3) INFRASTRUCTURE

According to this McKinsey Report India’s Eleventh 5-year plan envisages infrastructure investments of close to USD 500 billion with USD 430 billion of this in the core transport and utility sectors. About one fourth of this is expected to be met through Public Private Partnerships.

As the Government in India slowly opens up the infrastructure sector to private companies, the need for experts in this area is increasing.

“Be it building ports, roads, even nuclear plants, private companies are looking to hire individuals who have the experience in infrastructure development,” Juneja says.

Having said that, Lakshmikanth adds, “In this sector, companies are looking at experts from countries like Australia and not so much the US. The infrastructure development in the US happened a long time back. The more modern developments have happened in countries like Australia.”

4) E-COMMERCE

The entry of Amazon.com in India has cast away any doubts about the future of Ecommerce in India. This report says that some USD 3 billion worth of e-commerce was transacted in 201 And, according to Helion Venture Partners, USD 20 billion worth of e-commerce will be done in five to seven years, with 12-15% of shopping going online in this period.

“As Indian Ecommerce and deal companies like Flipkart, Snapdeal etc become popular there is an increasing need for people who have worked in Ecommerce environments – those who can create infrastructure to handle large traffic, build applications, enhance user experience etc,” says Lakshmikanth.

Companies in the US are far ahead in terms of Ecommerce, so as an NRI who has worked in that sector in the US, you will be much sought after in India.

5) INFORMATION TECHNOLOGY

While India continues to remain a hub for cost effective technology operations, certain niche technology operations still require global expertise.

“Technology companies in India for instance might be building a DNA sequencing program for multinational healthcare companies. The functional support for this program will most likely come from someone who has that kind of research background which is available in developed markets” Lakshmikanth says. Juneja too cites the example of pharma analytics as an area that needs expertise from developed markets.

Another area – large logistics and supply chain companies that use Indian technology companies to build their modules. “These companies typically need global experts to offer functional support,” Juneja says.

In addition to the above, smaller sectors in areas like wine making, gaming etc which are starting to become popular in India are hiring those with global expertise. According to some estimates, wine consumption in India is expected to grow by 25-30% annually between 2009 and 2012 and the Indian Gaming Industry is expected to grow at acompounded annual growth rate of 32% to Rs. 3,100 crore by 2014.

Contact us for further information at innovation@dieIdee.eu

Quelle: India Newsletter 02.2012 published by the Indian Embassy of Vienna

GettyAmazon VP of Echo Mike George.

GettyAmazon VP of Echo Mike George. TeslaTesla’s autopilot mode scanning the road.

TeslaTesla’s autopilot mode scanning the road.

{kind=link}